Summary

Super Micro Computer sells high performance server, storage, and networking solutions to enterprise customers. It’s a fast growing high tech firm carrying an unusually low valuation due to events in its past.

Manulife Financial Corporation is a highly profitable dividend-generating global insurance and financial services firm with a growing business in Asia, home of the world’s largest and fastest-growing middle class.

______________________________________________________________________

Super Micro Computer Inc. ($SMCI)

Source: tradingview.com

???? Summary:

- Share price at the time of writing: $91.98

- Super Micro Computer manufactures application-optimized, high-performance server, storage and networking solutions.

- $SMCI sells to specialized customers, including enterprise data centers, cloud computing, artificial intelligence, 5G and edge computing markets.

- The Company is the only major server and storage vendor that designs, develops, and manufactures most of its systems in the United States.

- Revenues and earnings have increased dramatically over the last two years, and valuation remains reasonable despite the recent share price surge.

???? What they do:

Super Micro Computer Inc provides highly sophisticated systems, including complete servers, storage systems, modular blade servers, blades, workstations, complete rack scale plug and play solutions, networking devices, system management software, and server sub-systems.

These products are offered in multiple models and configurations, allowing customers to select flexible solutions tailored to their needs.

$SMCI’s modular architecture allows it to incorporate new microprocessor, GPU, and other technologies rapidly, and the Company aims to be consistently the first to market with systems incorporating the latest developments.

Super Micro Computer employs over 1,800 people in R&D alone. The combination of aggressive R&D and in-house manufacturing enables fast prototyping and product roll-out.

$SMCI also offers software management solutions and a global services and support capacity.

Key product lines:

- SuperBlade® and MicroBlade™® system families designed to share common computing resources, saving space and power over standard rack-mount servers

- SuperStorage systems that provide high-density storage with efficient use of power to achieve performance-per-watt savings

- Twin family of multi-node server systems designed for density, performance, and power efficiency

- Ultra Server systems for demanding enterprise workloads

- GPU or Accelerated systems for AI markets

- Data Center Optimized server systems that deliver increased scalability and performance-per-watt with an improved thermal architecture

- Embedded (5G/IoT/Edge) systems optimized for evolving networks and intelligent management of connected devices

- MicroCloud server systems that deliver node density in environments with space and power constraints.

All of these systems are designed to minimize power consumption and waste and maximize operating efficiency.

Super Micro Computer has facilities in Taiwan and the Netherlands, but the primary manufacturing base is in San Jose, CA.

???? What we learned from social media and institutional investment patterns:

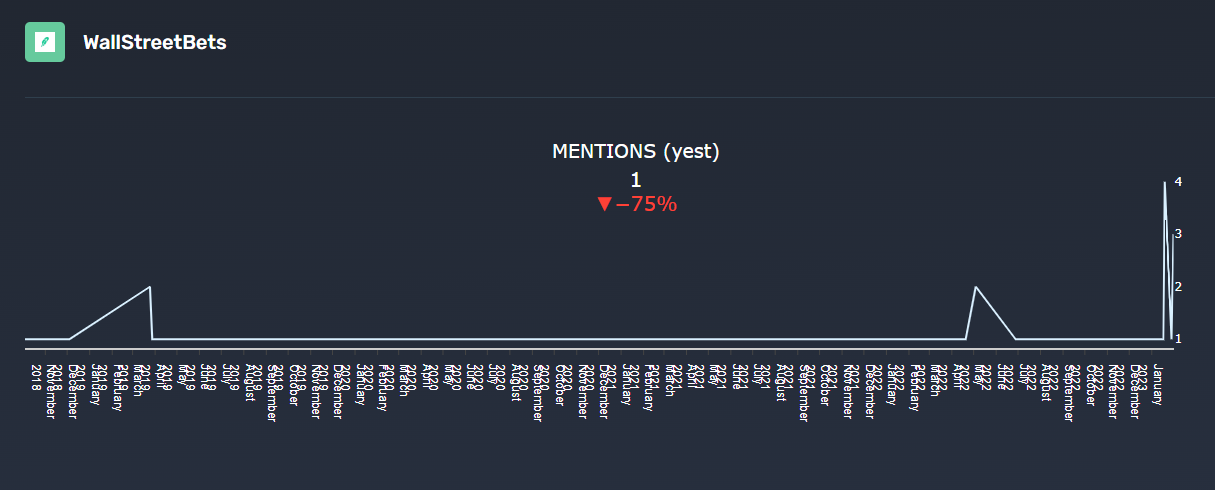

$SMCI is a cutting-edge tech manufacturer. That usually attracts some social media attention. In this case the attention is limited, possibly because the company is relatively small and serves enterprise customers almost exclusively, with no presence in the consumer technology market.

Engagement on r/wallstreetbets is generally low.

Source: quiverquant.com

There are sporadic mentions on r/stocks and other discussion groups, but posts are infrequent. Engagement has been generally low even when the stock price was soaring. A viral surge seems very unlikely.

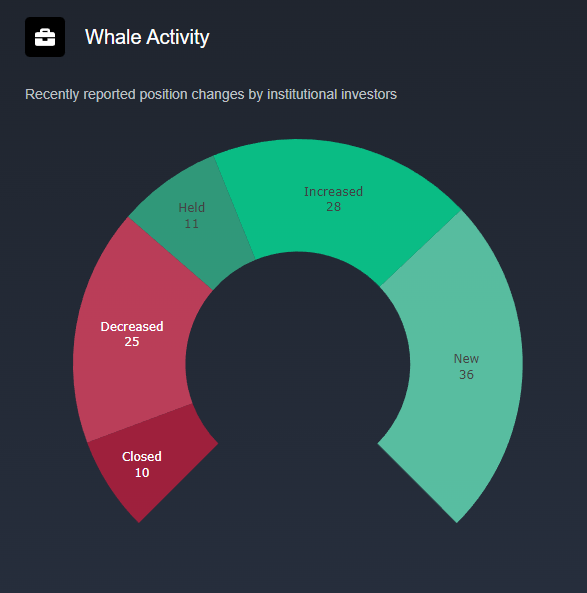

Insiders hold just over 13% of the shares, a fairly high figure. Institutions hold 92.6% of the float, which is relatively small at 46.8 million shares. 393 institutions hold shares, with Blackrock and Vanguard each holding just over 10% of the float.

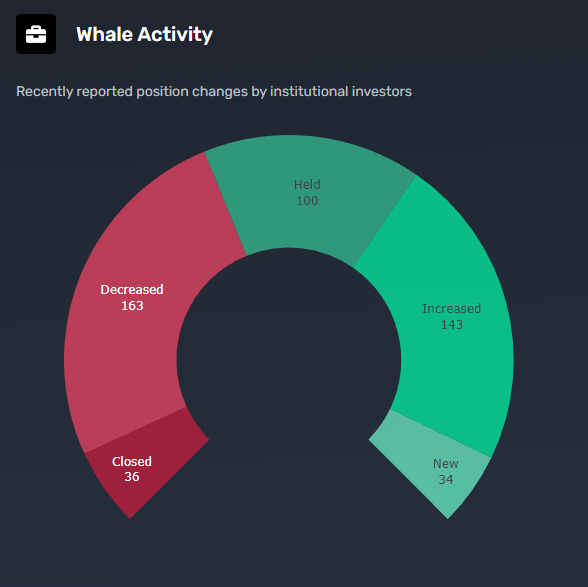

Institutional investors seem generally positive on the stock.

Source: quiverquant.com

The small float and high level of institutional ownership leave a relatively small number of shares available for retail investors. A modest level of buying or selling can move the stock significantly.

Notable comments from Reddit:

“Another point to consider is the proliferation of 5G… it allows remote computing power to be deployed into the world in ways that wouldn’t have been possible previously. 5G will allow massive data centers to take over more of the computational workload from local computers. More and more information will be processed and stored remotely. This could be quite the boon for a company that supplies the components of data centers.”

– MaxwellThePrawn

“I made lots of money with it and I'll hold long term. It's one of my winners in 2022 along with Clearfield and Enhpase Energy. Had to sell Enphase because the valuation got ridiculously expensive and carried too much risk but SMCI and Clearfield are still extremely cheap.”

– Most_Champion

???? Smart Money Signal: Jim Simons of Renaissance Technologies has bought 556,000 shares of $SMCI in the last two quarters.

???? Why $SMCI could be valuable:

Super Micro Computer operates in high-growth markets. The global server market is expected to grow at a CAGR of 7.8% through 2028. The data storage market is expected to show a CAGR of 17.8% through 2030, and the networking solutions market is projected to turn in a 20.5% CAGR through 2029.

$SMCI manufactures some of the most sophisticated enterprise solutions in the world, serving customers in fast growing industries where any technological edge can be a key competitive factor.

$SMCI is releasing a new Universal GPU system based on a unique building block approach, allowing their systems to support multiple GPU form factors, CPU choices, storage, and networking options. The system is designed to support fast, efficient deployment of artificial intelligence, machine learning, and high-performance computing applications.

SMCI manufactures its products primarily in the US, putting it in a position to benefit from bipartisan political moves to encourage domestic manufacturing, especially in the tech industry.

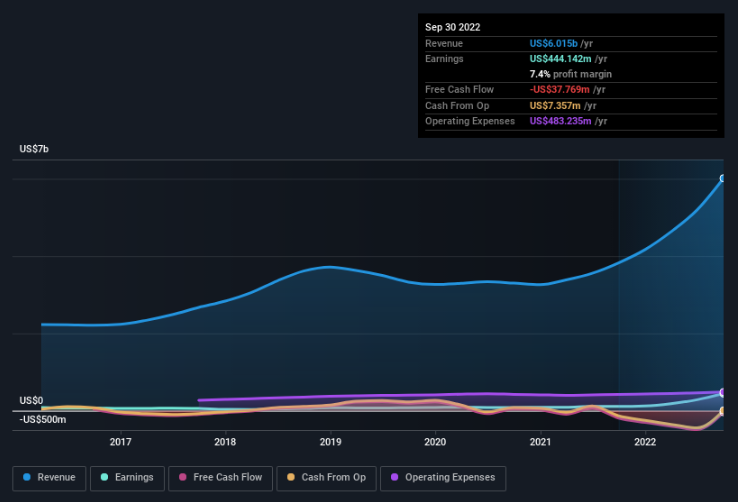

SMCI revenues have soared since 2021.

Source: Simply Wall Street

It’s important to note that SMCI’s customers are large tech-focused enterprises. They are not basing purchasing decisions on advertisements or celebrity endorsements. If they are buying SMCI equipment, it’s because they believe that it’s superior.

Revenue growth in the most recent quarter was 53.8% over the equivalent quarter last year. This is substantially faster than market growth, indicating that the company is gaining market share. SMCI expects revenue growth to average 17% to 23% through 2024, three times their market growth estimate of 7%.

Earnings are growing even faster than revenues.

| 2019 | 2020 | 2021 | 2022 | 2023* | |

| Diluted EPS | $1.39 | $1.65 | $2.19 | $5.32 | $9-$11 |

| % Growth | 18.7% | 32.7% | 143% | 69% – 106% |

*Analyst projection range, reported by Investing.com.

Operating margin is 10.39%, which is not exceptional. On the brighter side, margins have been improving steadily for the last two years. Return on equity is a solid 38.49%. The Company has more cash than debt.

$SMCI’s revenue and earnings growth have allowed the company to maintain highly competitive valuation ratios despite a 133% increase in the stock’s value over the last year. The Company trades at only 0.87 x trailing twelve-month sales and 8.5 x trailing earnings, less than half the peer average of 21.0. The price/earnings growth (PEG) ratio is only 0.76.

These valuations are low for a high-growth tech company, and it’s natural to ask why the market places such a low value on SMCI. The stock chart is also unusual: the stock price peaked in 2015 and slumped until 2021, a period when growth tech in general was booming, and soared in 2022, when growth tech overall was being hammered.

The explanations lie in the company’s history. There was a period when serious questions were raised about the accuracy of SMCI’s financial reporting, culminating in the failure to file their 2017 Form 10-K on time. This produced shareholder losses and ongoing threats of legal action. The Company cooperated fully with the investigation and reached a settlement with the SEC in 2020.

Despite governance reforms, investors remained wary and steered away from the stock for several years. It has only recently reached a position where investors are regaining trust and moving back in.

Because $SMCI has a relatively low float and the price responds quickly to even modest buying or selling action, it has been attacked in the past by short sellers who take a short interest, issue a highly negative opinion, and try to push the stock down.

⚠️ What the risks are:

1️⃣ Geopolitical risk. $SMCI manufactures primarily in the US but has invested heavily in a facility in Taiwan. Like almost all tech manufacturers, $SMCI relies in part on subassemblies and components from Taiwan. Conflict or threats of conflict over Taiwan could materially affect results.

2️⃣ Concentrated customer base. $MCI sells most of its products to a relatively small group of leading data center operators, cloud customers, OEMs, and similar large tech enterprises. This is a highly competitive business, and if even a few major customers move away from SMCI the impact on growth could be significant.

3️⃣ Governance risk. $SMCI experienced financial reporting issues in 2017 that acted as a drag on the stock’s price for years. Any recurrence or even perceived recurrence of these issues could have a severe impact on investor sentiment. Short sellers have exploited this vulnerability in the past and could do so again.

Bottom line: $SMCI is a turnaround play built on recovery from a series of past reporting problems that sent the stock to a level that, based on fundamentals, is undervalued despite its share price growth over the last year. The underlying business appears to be sound, the balance sheet is clean, and growth is strong.

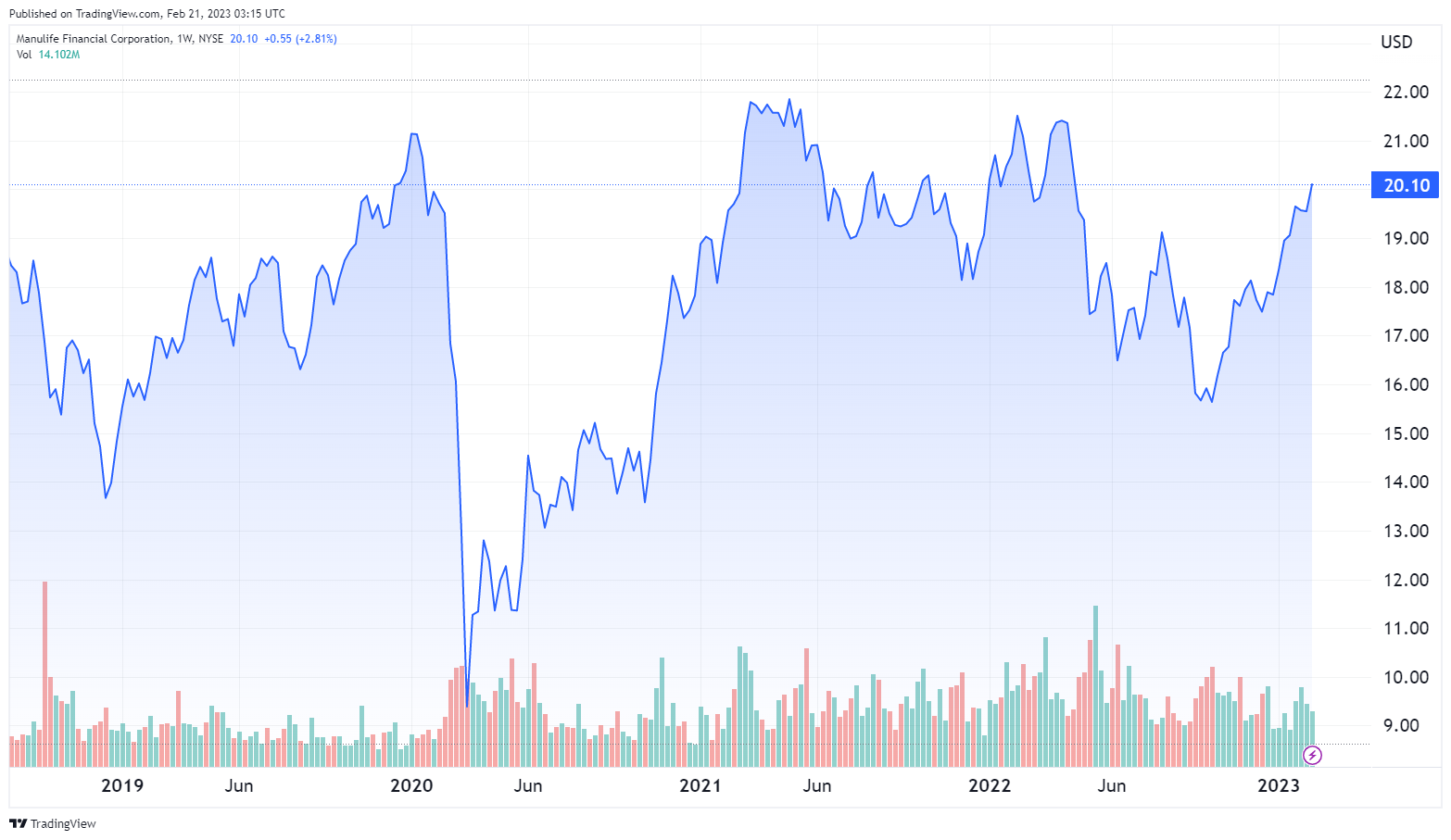

Manulife Financial Corporation ($MFC)

Source: tradingview.com

???? Summary:

- Share price at the time of writing: $20.10

- $MFC has established and solidly profitable operations in mature markets like the US and Canada.

- The Company has established a strong presence in Asia, where a fast-growing middle class drives rapidly increasing demand for financial products.

- $MFC offers an impressive 4.65% 5-year average dividend yield, and has increased its dividend an average of 11% per year since 2013.

???? What they do:

Manulife Financial Corporation is a multinational financial services group offering financial advice, insurance, and wealth and asset management solutions for institutions, groups, and individuals.

The Company operates under the Manulife brand in Asia, Europe, and Canada and under the John Hancock brand in the United States.

Manulife operates in five reporting segments, each with its own set of product and service offerings.

- Asia (43% of revenue): insurance products and insurance-based wealth accumulation products.

- U.S. (29% of revenue): life insurance products, insurance-based wealth accumulation products, in-force long-term care insurance, in-force annuities.

- Canada (19% of revenue): insurance products, insurance-based wealth accumulation products, banking services, inforce variable annuities.

- Global Wealth and Asset Management (20% of revenue): provides investment advice and solutions to retail, retirement and institutional clients under the Manulife Investment Management (“MIM”) brand.

- Corporate and Other: investment performance on assets backing capital, financing costs, costs incurred by the corporate office related to shareholder activities (not allocated to operating segments), Property and Casualty (“P&C”) Reinsurance, and run-off reinsurance.

$MFC was incorporated in 1887 and is headquartered in Toronto, Canada. Shares are traded on the NYSE, the TSX, and exchanges in Hong Kong and the Philippines.

???? What we learned from social media and institutional investment patterns:

$MFC is very much an old school investment, and it’s not the type of company that generates significant social media buzz. Mentions on r/wallstreetbets are almost nonexistent.

Source: quiverquant

There is some discussion on other forums, but very little of it is exclusively devoted to $MFC. Most mentions are in the context of wider discussions of Canadian stocks, dividend stocks, or insurance stocks. The few posts with stock research generate minimal engagement.

It’s safe to say that $MFC will not “go viral,” and social media discussion is not likely to generate significant buying or selling action.

An unusually low 52.6% of the float is held by institutions. Canadian institutions, led by the Royal Bank of Canada, dominate the list of major institutional holders, though Vanguard is the second-largest holder with 3.77% of the float.

Recent institutional activity seems generally positive, though not by a wide margin.

Source: Quiverquant

???? Smart Money Signal ???? Jeremy Grantham of Grantham, Mayo, & van Otterloo has purchased 2.6 million shares of $MFC in the last three quarters.

???? Why $MFC could be valuable:

Insurance and financial services in mature markets are traditionally low-growth markets, with major companies characterized by solid profitability and good dividends rather than exceptional growth rates. With a 66.23% operating margin, $17.7 billion in operating cash flow, more cash than debt, and a 4.65% five year average dividend yield, $MFC fits this model.

$MFC adds an additional element to this combination. The Company has invested heavily in emerging Asia, where it has established an early foothold in multiple markets: China, Indonesia, Japan, Singapore, Taiwan, Malaysia, Vietnam, the Philippines, Cambodia, and Myanmar.

This region is home to a large percentage of the world’s population. It also has a large and growing middle class – China’s middle class alone is twice the size of the entire US population – that is a natural market for insurance and financial services.

Established Western brands are well regarded in this market, and Manulife’s early entry to the market has placed it in a strong competitive position in a market with potential for significant growth.

As a Canadian company, $MFC is less likely to be hampered by trade disputes with China than an American counterpart might be.

Despite persistent COVID-19 headwinds in the Asian market, $MFC has generated consistent earnings growth.

| 2019 | 2020 | 2021 | 2022 | |

| Diluted EPS* | 2.77 | 2.93 | 3.54 | 3.68 |

*Canadian Dollars

$MFC’s Price/Book Value ratio is only 0.96, meaning the company’s stock price is less than the per-share value of assets minus liabilities. The industry average is 1.37. The Price – Cash Flow (PCF) ratio is 6.59, well below the industry average of 10.

The trailing P/E ratio is 7.22, less than half the peer average.

$MFC repurchased 79 million common shares in 2022, demonstrating a commitment to shareholder value.

$MFC’s dividend is a strong part of the stock’s appeal. The current forward annual dividend yield is an exceptional 5.51%, and the average yield over the last five years is 4.65%. The payout ratio is a highly sustainable 35.87%, and the average annual dividend increase since 2013 has been 11%.

⚠️ What the risks are:

1️⃣ Geopolitical risk. $MFC’s Asian exposure provides a growth opportunity that’s lacking in mature markets, but it also exposes the Company to significant risk in the event of sanctions, tension or conflict, particularly between China and Taiwan. .

2️⃣ Climate and Natural Disaster Risk. Manulife’s preperty and casualty reinsurance business, as well as their life insurance business, could see significant losses if the risk of natural disaster is not effectively assessed and priced into premiums. $MFC also has significant investment exposure to the oil and gas industry, which could be negatively affected by increased regulation.

3️⃣ Regulatory risks. $MFC operates in numerous jurisdictions with different regulatory regimes applying to insurance and investment management, including different insurance regulations in all 50 US states. Compliance issues or regulatory actions could directly affect the Company’s results and reputation.

Bottom line: Manulif Financial Corporation companies mature-market stability and profitability with an opportunity for significant growth in the Asian market. The strong profitability, solid balance sheet, and exceptional dividend combine with attractive valuation ratios to create an attractive package for risk-averse value investors.

That's a wrap!

Don't miss our next report. If you haven't already make sure to whitelist this email so we don't end up in your promotions folder. Not sure how to do it? Use this guide.Got 15 seconds? To make sure we can keep improving Ticker Nerd we need to hear from you. We have a few quick questions for you here.