Summary

Public Storage is the largest provider of self-storage space in the US. The company is expanding rapidly and growing revenue and earnings, while the share price remains depressed

Airbnb Inc. is the dominant online marketplace for vacation rentals. The Company is solidly profitable and delivered a record-setting quarter in Q3 2022 and has bounced back strongly from the pandemic-driven travel shutdown.

______________________________________________________________________

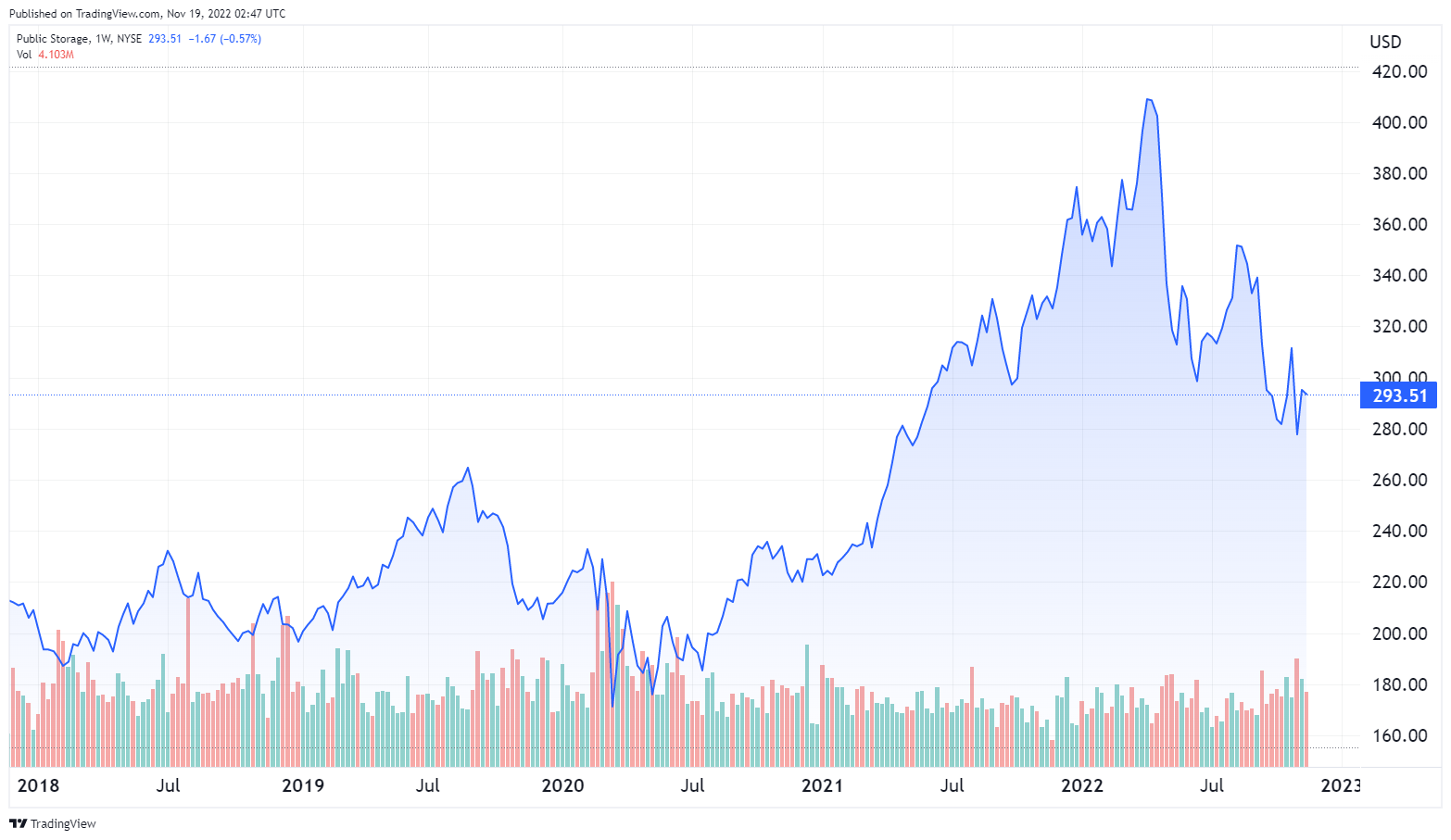

Public Storage Inc. ($PSA)

Source: tradingview.com

???? Summary:

- Share price at the time of writing: $293.51

- Public Storage is the largest self-storage REIT in the US, with 186 million square feet of rental space in 39 states.

- Since 2019 $PSA has added 26 million square feet of new storage space.

- Public Storage has shown consistent growth in revenue and funds from operations (FFO)

- $PSA shares are trading at 30% below recent peaks despite consistent strong financial performance.

???? What they do:

Public Storage is a Real Estate Investment Trust (REIT) specializing in self-storage space. The Company has been in business for 50 years and is the largest self-storage REIT in the country.

Like all REITs, Public Storage is required to distribute 90% of its taxable income to shareholders as dividends.

Public Storage operates in three business segments.

- Public Storage operates 2,787 self-storage facilities in the US, with 198.319 million square feet of space.

- Shurgard Self Storage SA (SHUR.BR) has 253 facilities with 13.799 million square feet of space in seven Western European countries. $PSA owns 35% of Shurgard

- Orange Door, an ancillary brand of Public Storage, provides tenant reinsurance and other related services.

The US operations of the Public Storage brand generates a large majority of the Company’s income.

Up until July 2022 Public Storage also managed commercial properties, through a 41% interest in PS Business Parks Inc, which owns 27.7 million square feet of space in six states. Public Storage sold this interest to affiliates of Blackstone Real Estate for $2.7 billion in April 2022. The sale allows $PSA to focus on its core self-storage and ancillary services businesses.

Public Storage has moved aggressively to leverage technology in support of a traditional business.

- eRental is a digital lease that allows customers to rent online and move in themselves. It accounts for 50% of move-ins.

- Digital Property Access Systems allows direct access to parking gates, doors, and elevators through the Public Storage app.

- Comprehensive mobile app: the highly-reviewed app provides full leasing, account management, customer service, and access functions.

These innovations reduce overhead and provide a superior customer experience, allowing customers to rent and access storage space entirely through the app..

Public Storage added 240 properties with a total of 23 million square feet of storage space in 2021, using acquisitions, development, and redevelopment.

Expansion is continuing in 2022. Since June 30 $PSA has acquired or is under contract to acquire 24 self-storage facilities with 1.7 million square feet of rentable space.

???? What we learned from social media and institutional investment patterns:

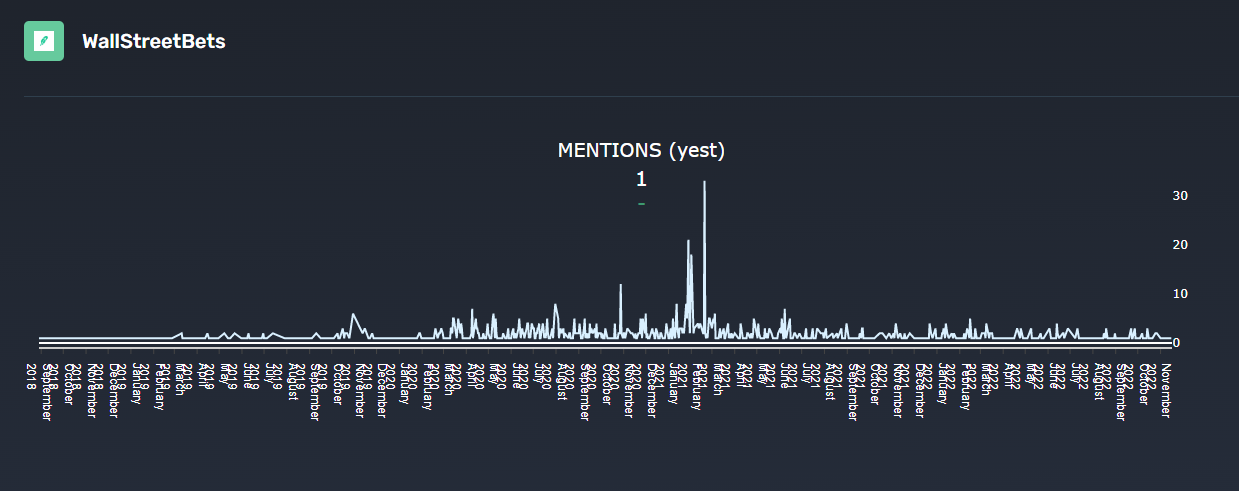

$PSA sees minimal discussion on Reddit, and what little there is can be found as general discussion of REITs and dividend stocks.

This is not surprising. Most REITs are classic “boring stocks”, they aren’t likely to go “to the moon” or experience viral trading. They are not household names or purveyors of the latest technology.

Source: quiverquant.com

There are a few posts on r/stocks and the discussion is generally positive, but there’s too little of it to draw any conclusions. It is reasonable to assume that price movements will not be driven by social media buzz.

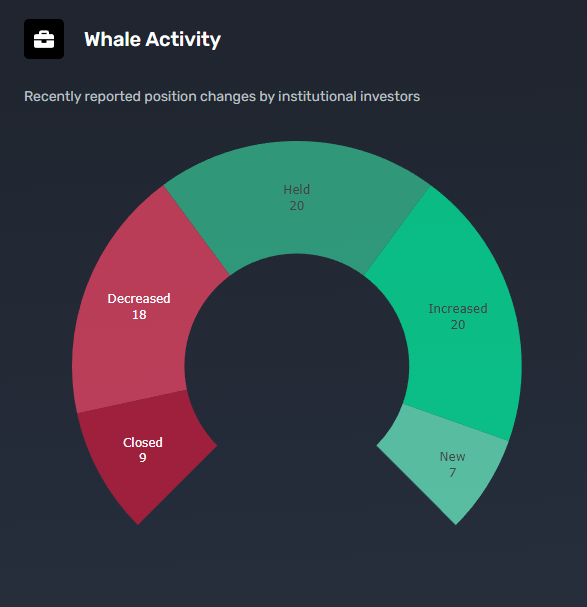

13.58% of $PSA shares are held by insiders, a relatively high figure. 94.01% of the float is held by institutional investors, led by Vanguard and Blackrock. Recent institutional activity has been generally positive:

Source: quiverquant.com

Notable comments from Reddit:

“I have owned them for years and think they are a good buy because people use them in good times and in bad times. When downsizing, for example, people store all their stuff there that won't fit in their new place.

They are also updating their existing facilities to be non-staffed and I'm sure they will keep at this as much as humanly possible. This means that you enter a code to get into the gate, and then enter your code to unlock your storage space, rather than deal with an employee. Having a business that works just fine with no staff on site is incredible and the more they change to be like this, the more profit they will make.”

– kezlorek

“I work for a marketing firm and our biggest client is a self storage company that competes directly with Public Storage. PSA is by far the most popular self storage company on the market. I deal with the pay per click metrics daily and see it myself. I’d go with PSA.”

– WjorgonFriskk

???? Smart Money Signal: Ken Griffin of Citadel has purchased 191,000 shares of $PSA in the last two quarters. Ray Dalio has bought shares in the last four consecutive quarters.

???? Why $PSA could be valuable:

The self-storage market is expected to show a CAGR of 7.53%% through 2027.

Self-storage is traditionally a recession-resistant business, as financially stressed individuals and households move to smaller, more affordable accommodations and look for places to store their belongings. During the 2008-2009 recession, when most commercial real estate saw a 25% to 67% drop in earnings, self-storage saw a 5% gain.

The self-storage market is highly fragmented, with nearly 75% of the market in the hands of small local operators. Size and nationwide reach give Public Storage a substantial advantage. They have the financial capacity to drive acquisitions, property expansion, and property development, and to invest in automated systems that reduce overhead and enhance customer appeal.

The nationwide reach and financial capacity of Public Storage also allow advertising and brand-building on a national scale, something few competitors can match.

Public Storage has invested heavily in technology. As a result, customers can rent space, manage their accounts, and gain secure access to their storage units entirely through a dedicated app. No competitor can match this capacity.

Public Storage has used acquisitions, site expansion, and new site development to expand its total US rental space from 2,429 facilities with 162.047 million square feet of rentable space at the end of 2018 to 2,787 facilities with 198.319 million square feet of rentable space at the end of 2021.

Expansion has continued in 2022: in the third quarter $PSA acquired 24 facilities with 1.7 million square feet of storage space and gained another .5 million square feet from internal development. As of Sept 30, 2022, the Company had 5.1 million square feet of new projects in development.

$PSA’s occupancy rate is currently 94.5%. This is down from 96.8% a year earlier, probably due to the addition of new space, but it remains a very strong figure. An excessively high occupancy rate is not entirely positive, as it leaves no room to accommodate new customers.

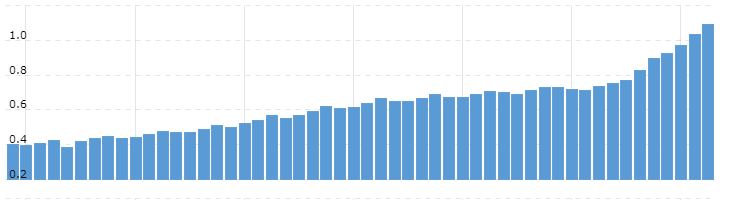

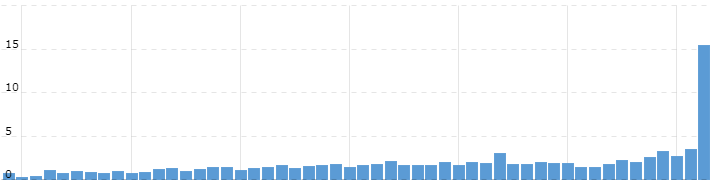

Public Storage revenues have increased consistently, both from same-facility growth and from the addition to new facilities. Same-store net operating income (NOI) was up 17% from the previous year in Q3 2022. Core funds from operations (FFO) a metric frequently used by REITs, increased 20%

Quarterly Revenues (billions):

The surge in EPS is due to the sale of the Company’s 41% interest in PS Business Parks, and will not be repeated.

$PSA boasts an impressive operating margin of 51.1%, with ROE at 47.74%. The Company has a solid cash position, and while it carries substantial debt, like most REITs, its debt-to-equity ratio is lower than that of most competitors. The Company has the capacity to sustain it’s acquisition and development program.

$PSA earnings have beaten consensus analyst estimates for four consecutive quarters.

Shares are trading at 30% below their April 2022 peak despite strong financial performance. The dividend yield currently stands at 2.73%.

18 analysts currently cover $PSA, with a consensus “Buy” rating and an average price target of $359.08, 22.34% above the current price.

⚠️ What the risks are:

1️⃣ A substantial debt load. The Company’s long-term debt load has grown from $1.9 billion at the end of 2019 to $6.74 billion in the most recent quarter. This is a typical pattern for REITs, which rely on debt to acquire and expand properties. Rolling over debt could still be a challenge as interest rates rise, especially if the acquisitions are less profitable than expected.

2️⃣ Data security and privacy risks. The move to tech-driven systems reduces costs and appeals to customers, but it produces risks. Any data breach leading to the release of customer data or the theft of property could have a serious impact on the Company’s credibility and on customer trust.

3️⃣ Development risk. $PSA is aggressively developing new self-storage facilities. Costs may exceed projections, and the space in these facilities is not pre-leased. Development decisions are based on projected demand and the projections may not be accurate.

Bottom line: Public Storage is a conservative, recession-resistant dividend-bearing REIT with a strong financial position. It’s a defensive investment ideally positioned to weather economic storms.

Airbnb ($ABNB)

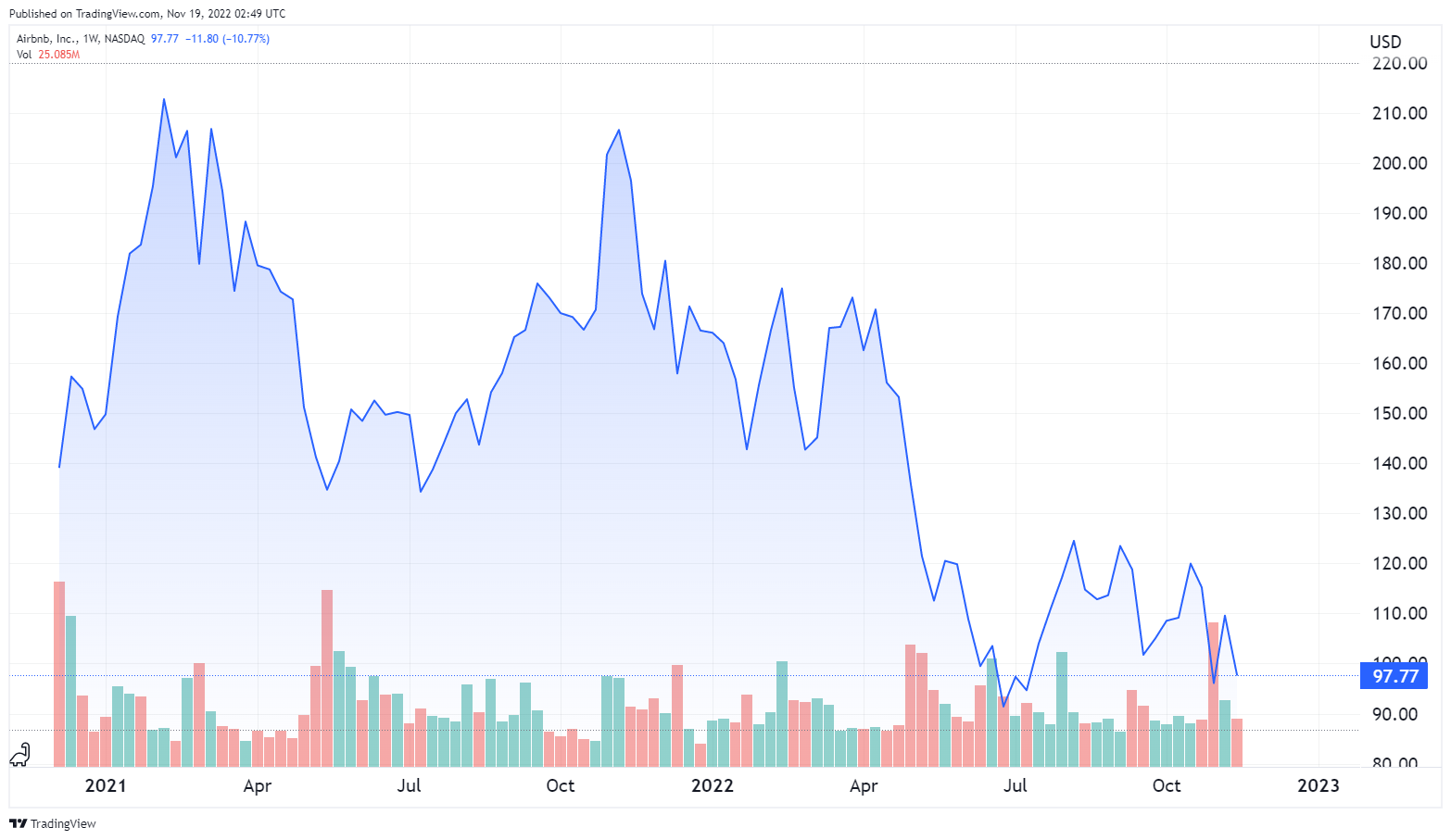

Source: tradingview.com

???? Summary:

- Share price at the time of writing: $97.77

- Airbnb operates a platform linking providers of accommodation and experiences with guests worldwide.

- $ABNB delivered record revenue and earnings results in Q3 2022.

- The share price has fallen almost 53% in the last year despite steadily improving performance.

???? What they do:

Airbnb is a platform linking providers of experiences and accommodations (including rooms, apartments, and houses) with guests. The platform operates globally and has become a household name.

Airbnb opened in 2007, primarily as a way for people to rent spare rooms to visitors. The concept grew rapidly and today hosts offer rooms, apartments, houses, boats, castles, and almost any other accommodation anywhere from urban centers to remote rural areas.

Airbnb also offers experience hosting, which is limited only by the imagination of the providers.

Airbnb hosts have welcomed over a billion total Airbnb arrivals. The Company currently has around 6 million listings, offered by over 4 million hosts in over 100,000 cities and towns in over 220 countries. Listings encompass an enormous range of prices and locations.

In 2021 $ABNB derived 54% of its revenue from North America, 32% from Europe, the Middle East, and Africa, 7% from the Asia/Pacific region, and 7% from Latin America.

Airbnb charges hosts a flat 3% fee and guests pay from 6% to 12%, with Airbnb taking an average of 13% of the gross booking value. The Company has its own payment platform and an extensive suite of security features designed to protect both hosts and guests.

Airbnb effectively invented its niche and is the dominant player in it.

Airbnb went public through an IPO on Dec 10, 2020 and has been a publicly traded company for just under 2 years.

???? What we learned from social media and institutional investment patterns:

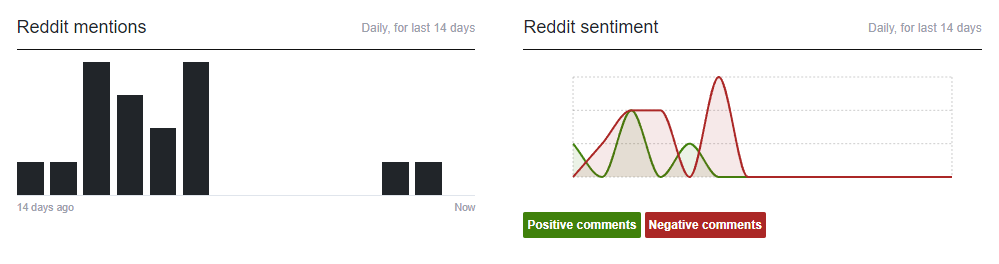

Airbnb is visible on Reddit but the current activity level is anything but viral. Investor sentiment is mixed.

$ABNB is the type of company that often gets attention on social media: it’s relatively new, has the “disruptor” label, and has shown strong growth with a long runway ahead. It’s still receiving relatively minimal attention.

This appears to be partly driven by a generally subdued environment for investment discussion on Reddit: the bear market has substantially reduced posting volume across the board.

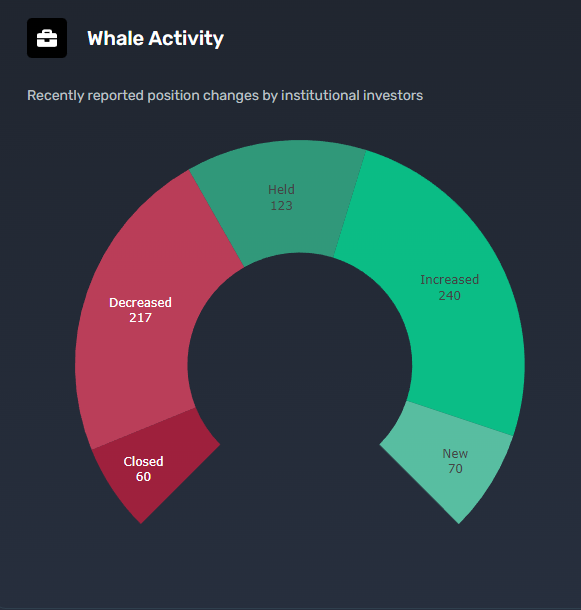

Airbnb has a relatively low level of institutional ownership. Recent institutional activity shows a generally positive trend:

Source: Quiverquant

Notable comments from Reddit:

“Their numbers don’t show much reason to be bearish. Their earnings and growth are generally good if not great. 3 EPS beats in a row, barely missed revenue last quarter is a horrible macro environment, 67% revenue growth YoY. If this quarter shows something different I may change my tune, but I just don’t see much of a bear thesis. Also worth noting that United beat today, bullish for hotels/travel. While the stock is not cheap, but it is trading under its historical valuations. Adding around $80–$90 isn’t a bad idea IMO.”

– datcommentator

“I’m an Airbnb host. I’m bullish on the company overall, but bearish near term. The Pe is going to compress as we go into a recession and less people are traveling. Hard to time the market but I’d bet q1 2023 might be a great time to buy”

– dajuhnk

???? Smart Money Signal ???? Jim Simons of Renaissance Technologies has purchased 4 million shares of $ABNB in the last two quarters.

???? Why $ABNB could be valuable:

The global vacation rental market, including homes, apartments, resorts/condominiums, and others, is expected to show a CAGR of 5.3% through 2030. Online bookings are expected to show a higher CAGR of 6%. 70% of the vacation rental market was offline in 2021, offering abundant room for growth as younger users move into the market.

As the dominant player in the online vacation rental booking niche, Airbnb is well positioned to benefit from this expanding market.

Unlike hotels, Airbnb does not need to build or acquire facilities to add rooms. They just need to attract more hosts. The hosts provide and maintain their own properties, limiting both the Company’s need for CAPEX and operating expenses.

Airbnb has bounced back strongly from a pandemic-hit losing year in 2020. The recovery has been driven both by pent-up demand for travel and a move toward remote workers renting for longer terms to combine work with travel.

Over 90% of Airbnb’s website traffic is direct or unpaid, meaning that the Company is not spending to bring in users. That is the prerogative that goes with being a dominant and instantly recognizable brand, and it’s something competitors can’t match. People don’t say “I’ll book an online vacation rental”, they say “I’ll book an Airbnb”.

$ABNB delivered the highest revenue and earnings figures in company history in Q3 2022. Revenues were up 29% over the equivalent quarter in the previous year, driven by a 25% jump in nights and experiences booked. Net income soared 46% to $1.2 billion and free cash flow was up 81%. Without the impact of currency rate fluctuations, revenue would have gained 36% and income 61%.

Airbnb is a cash machine: free cash flow is up 519% since Q2 2021, while revenue is up 137.7% over the same period. The Company has effectively no debt: the total debt of $2.36 billion is a fraction of its $9.36 billion cash hoard.

This strong cash position has allowed extensive share buybacks, compensating for dilution due to outstanding warrants and shares issued to employees. It also leaves the Company well-positioned to weather any short-term downturn in bookings if the economy slips into recession.

While a recession could reduce booking volume and temporarily affect results, it could be a long-term positive. $ABNB has solid margins and cash that vastly exceeds debt, placing it in a great position to weather a recession more effectively than its competitors and emerge even more dominant.

Airbnb has responded to complaints from both hosts and guests by rolling out new features, including upfront notice of all fees, better verification of identities, and measures to prevent guests from booking properties and using them as party venues.

Revenue from the Asia-Pacific region grew 65% in Q3 2022. The region presents an enormous growth opportunity. Airbnb no longer has direct listings in China, but it attracts increasing numbers of bookings from Chinese citizens traveling outside the country. These bookings could increase dramatically as China pares back COVID-related travel restrictions.

Operating margin and ROE are strong at 20.56% and 32.61% respectively. Valuation measures suggest that the stock is not cheap: the trailing P/E is 40.57 and price-to-sales is 8.15. The stock is still trading far below its recent peaks and the growth rate and dominant competitive position in a growing industry suggest that the valuation is reasonable.

$ABNB is covered by 40 analysts. 6 rate it “Strong Buy”, 11 say “Buy”, and 21 say “hold”. The average price target is $133.65, 36.7% above the current price.

⚠️ What the risks are:

1️⃣ Economic uncertainty. A serious recession could lead to global cutbacks in leisure travel, affecting Airbnb’s bookings and results.

2️⃣ Security concerns. Airbnb’s business model presents unique security threats for both hosts and guests. Incidents or complaints involving Airbnb hosts or guests are likely to be highly publicized and could have a material impact on performance.

3️⃣ Saturation in key markets is a continuing concern. Large numbers of new hosts entering the market may result in reduced bookings and lead many hosts to leave the market. Concerns about active housing stock being diverted to short-term rentals could also lead to increased regulation in some markets. Either trend could have an impact on results.

Bottom line: Airbnb has an overwhelming competitive advantage as the originator and dominant player in a rapidly expanding niche. The Company’s growth rate, solid profitability and very strong cash position leave it well placed to manage any economic downturn and emerge in a better position than its competitors..

That's a wrap!

Don't miss our next report. If you haven't already make sure to whitelist this email so we don't end up in your promotions folder. Not sure how to do it? Use this guide.Got 15 seconds? To make sure we can keep improving Ticker Nerd we need to hear from you. We have a few quick questions for you here.