Summary

American International Group (AIG) is a major global Property & Casualty insurance company. It has sold off its less profitable units and built increasing profitability in its core business, and currently offers a compelling combination of value and growth.

Suncor is both Canada’s leading oil company and Canada’s leading hydrogen producer.

______________________________________________________________________

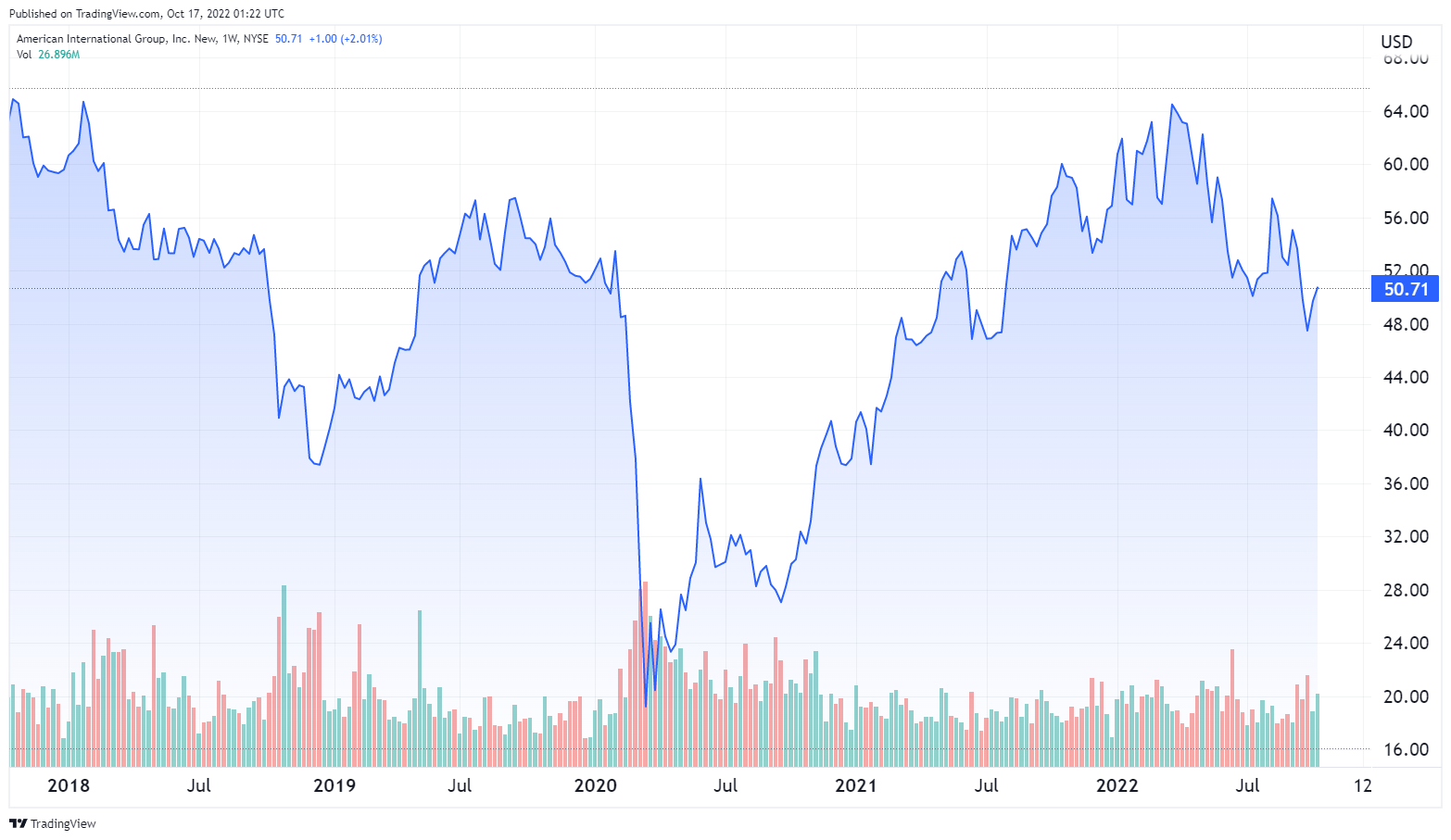

American International Group Inc. ($AIG)

Source: tradingview.com

???? Summary:

- Share price at the time of writing: $50.71

- AIG is one of the five largest insurance companies in the US by assets.

- AIG carved out its life insurance and asset management units in the largest IPO of 2022 to date, retaining majority ownership.

- The Company is aggressively repurchasing shares and pays a solid 2.5% dividend, channeling profits to shareholders.

- Revenue and earnings growth have bounced back strongly from a weak year in 2020. Valuation ratios, margins, and ROE are all very solid.

???? What they do:

AIG was founded in 1919 and is one of the oldest and largest insurance companies in the US. It is a global company, operating in roughly 70 countries. In 2021 13.6% of AIG premiums were written in Japan and 6.9% in the UK.

AIG was for many years an insurance conglomerate, with operations across the insurance spectrum. In 2015 AIG announced a plan to divest some units and transform itself into a more focused Property & Casualty (P&C) insurance company. As part of this strategy, AIG sold United Guaranty Corporation to Arch Capital (NYSE:ACGL) for $2.2 billion in cash and $1.225 billion in $ACGL shares.

AIG took another major step toward its goal in Sept. 2022, carving out its Corebridge life insurance and asset management unit in the largest IPO of the year to date. The IPO raised $1.68 billion and left AIG with majority ownership of the $13.6 billion company.

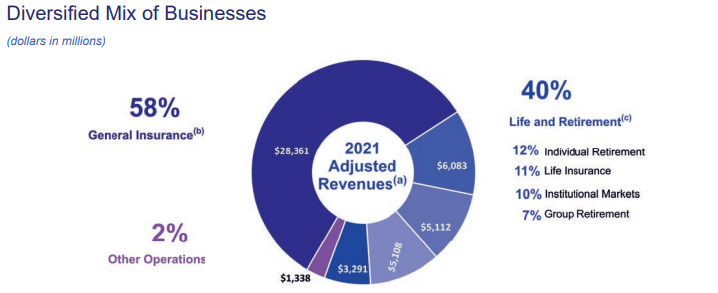

Before the Corebridge divestiture AIG’s general insurance division (which is now the company’s remaining business) represented 58% of the Company’s revenues.

While General Insurance represented 58% of AIG’s revenues before the Corebridge divestiture, it produced almost 74% of AIG’s pretax income in 2021. AIG has retained the most profitable portion of its business and sold off the portions that are earning less.

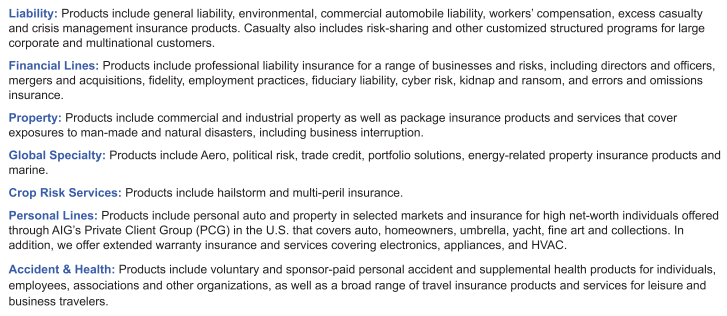

AIG’s General Insurance business, which now dominates the Company’s operations, is divided into US and Global segments. Each segment offers a similar range of products and services.

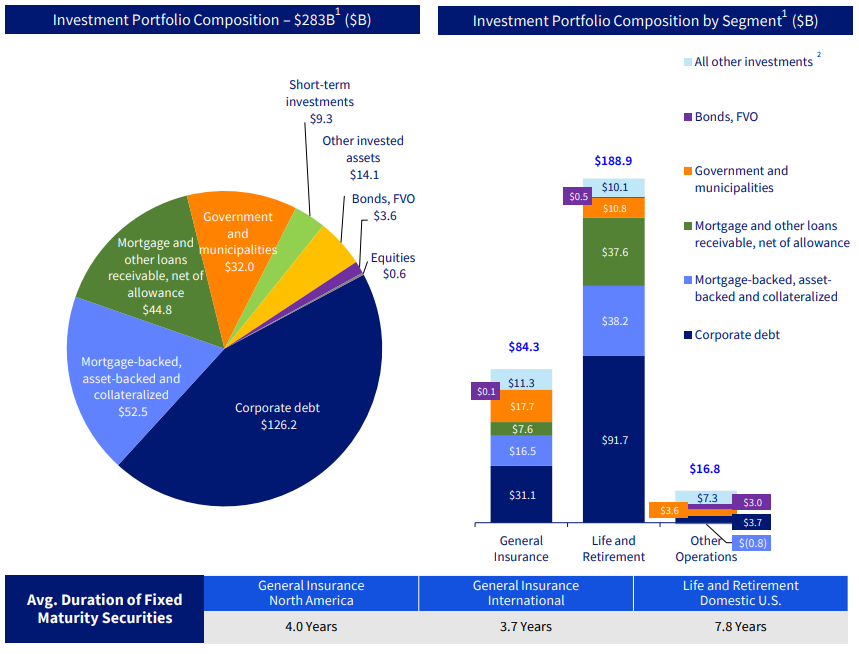

Like most insurance companies, AIG invests its insurance float: the difference between its income from premiums and its payouts on claims, AIG’s float is invested primarily in fixed-income securities.

This focus leaves rhe company less exposed to market fluctuations than competitors with higher exposure to equities.

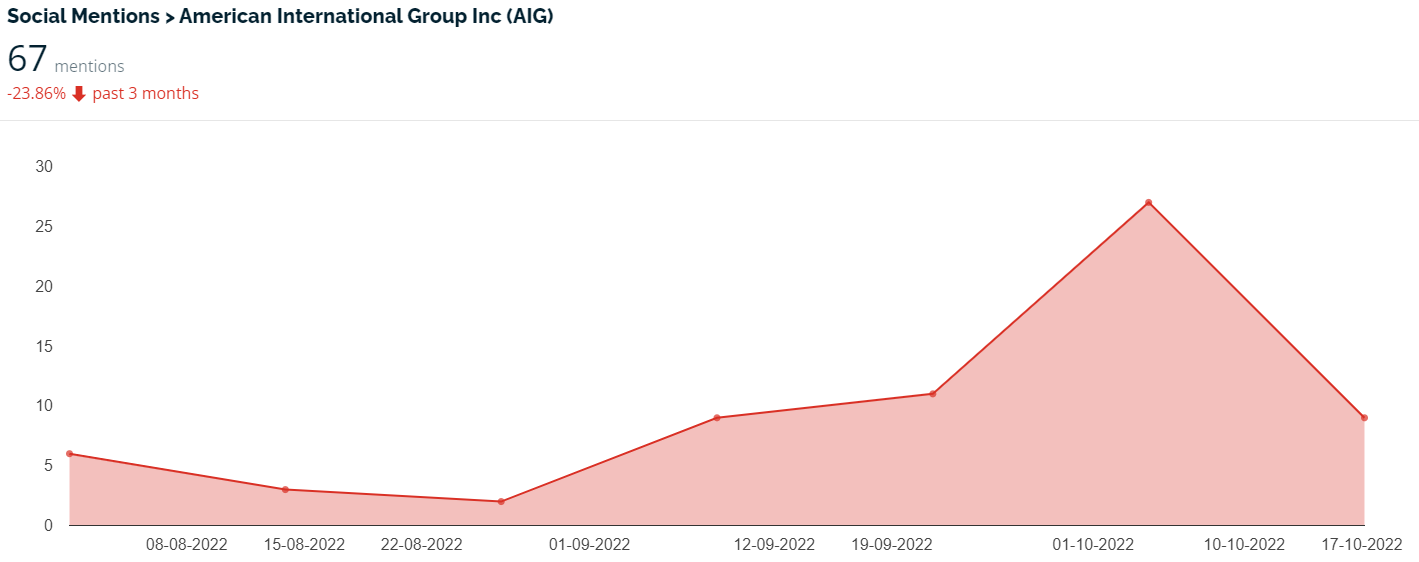

???? What we learned from social media and institutional investment patterns:

AIG has experienced a minor surge in social media interest beginning with the Corebridge IPO:

Source: marketsentiment.com

It’s not clear that this is driven by an interest in AIG as an investment or general discussion surrounding the IPO.

Over time, though, retail investor interest – at least on r/wallstreetbets – is extremely low:

Source: quiverquant.com

Searches for specific posts turn up few recent threads and the ones that do turn up are overwhelmingly negative. Much of the negativity stems from the 2009 financial crisis. AIG bet heavily on mortgage-backed securities and was one of the “too big to fail” companies that received a large government bailout.

AIG eventually paid back everything it received, but the negative sentiment remains.

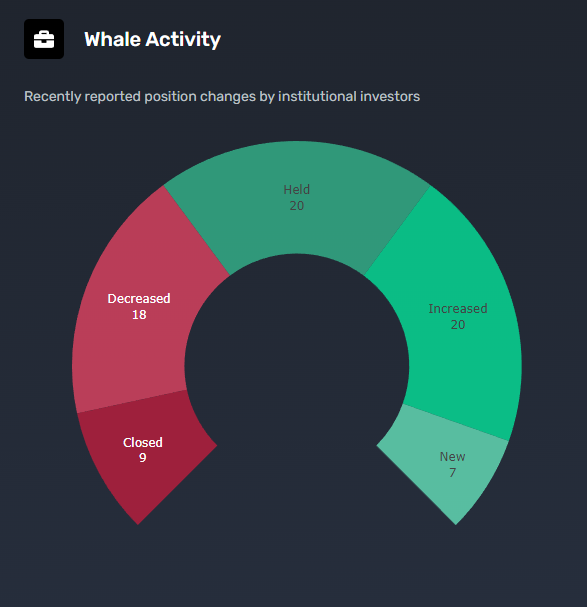

Institutional investors have no such qualms, and the general trend is to add to positions:

Source: quiverquant.com

Institutional owners control 93% of ther AIG float, led by the usual suspects: Vanguard, Blackrock, and T. Rowe Price.

???? Smart Money Signal: Ray Dalio has bought 243,000 shares of $AIG in 2022, and Steven Cohen of Point72 Asset Management has purchased 481,000 shares in thre last two quarters.

???? Why $AIG could be valuable:

The global insurance market is expected to show a CAGR of 9.1% through 2026. Swiss Re Institute predicts rising demand for insurance, citing “rising risk awareness, increasing demand for protection and rate hardening in non-life insurance commercial lines.”

P&C insurance is expected to show “one of the fastest growth rates” in the overall insurance landscape.

The Corebridge IPO allows AIG to focus on the most profitable segment of its business, and leaves it with a potentially very valuable 78% stake in Corebridge, currently worth around $10 billion at the current market’s depressed valuation.

It’s not clear whether AIG intends to sell the Corebridge shares gradually on the open market, distribute shares directly to AIG shareholders, or simply retain the stake. In any of these cases the Corebridge stake remains a valuable asset.

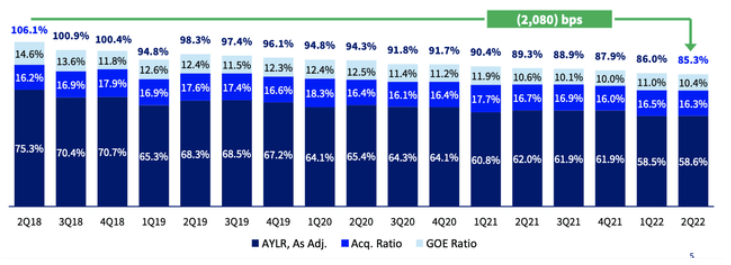

Insurance companies have two ways of making money. The first is through underwriting profits: the difference between the premiums they take in and the claims they pay out. This is measured by a percentage called the combined ratio. If the combined ratio is over 100 the company is losing money, if the combined ratio is below 100 the company is making money. The lower the ratio, the more money the company is making.

AIG’s combined ratio has been declining steadily since 2018 and now stands at 85.3, meaning the Company earns $14.70 annually for every $100 in premiums.

The improvement indicates stronger underwriting standards and improving risk assessments. That in turn indicates increased competitiveness: companies under competitive stress have to offer more insurance for less money, which tends to raise the combined ratio.

Total underwriting income in Q2 2022 was $799 million, up from $463 million in the equivalent quarter a year ago.

The elevated threat of natural disasters can be both a positive and a negative for AIG. Greater threats typically result in greater demand for P&C insurance and higher premiums. On the other hand, if underwriting standards and risk assessment are not adequate, the Comapny can be exposed to unusually large claim volumes.

AIG’s global customer base reduces its exposure to area-specific disaster risks.

The second way insurance companies make money, as anyone who follows Warren Buffett knows, is by investing their float: the money that they hold to cover claims.

Like most investors, AIG has lost money on its equity holdings in 2022: around $43 million so far. Because AIG holds mainly fixed-income investments, their exposure to stock market losses is relatively low. The company stands to gain substantially for rising interest rates: most of its holdings are short-term instruments that can be rapidly rolled over into higher-interest bonds as rates rise.

AIG has aggressively repurchased shares, reducing its outstanding shares from 859.4 million in Q1 2021 to 771 in Q2 2022. Management expects to further reduce this to between 600 and 650 million. There’s a solid 2.5% dividend and the payout ratio is entirely sustainable at only 8.4%.

Valuation ratios are extremely attractive, with the trailing P/E at only 3.15 and price/sales at 0.70. The operating margin is strong at 29.33% and return on equity is 24.43%.

Growth is difficult to quantify in a truly relevant manner because all past data include results from the now separate Corebridge units and because 2020 results were distorted by the pandemic. Revenues are still substantially up and 2021 diluted EPS stands at $10.82, up from $3.74 in 2019.

Underwriting income in the General Insurance segment, which does not include the Corebridge unit, increased from $294 million in Q2 2022 to $393 million in Q2 2022.

19 analysts currently cover AIG, with a consensus rating between “Buy” and “Hold” and an average price target of $64.75, over 27% above its current level.

AIG is essentially a turnaround story. The Company was faced with bankruptcy in 2008 after excessive investments in mortgage-backed securities and other cvollateralized debt obligations.

AIG was judged to be “too big to fail”, and received a $150 bailout package composed of loans and share purchases. The deal was controversial and generated enormous amounts of bad publicity for AIG. All the loans were eventually paid and the government has sold all of its shares, and in total the government made a $22.7 profit on the deal.

AIG still emerged from the controversy as a deeply damaged brand, and the negative connotations have contributed to retail investor aversion.

AIG currently trades at 31.x trailing earnings, compared to an industry peer average of 15.2x trailing earnings. This depressed value appears to be largely driven by residual negative perceptions from past problems, and could be perceived as a compelling value proposition.

⚠️ What the risks are:

1️⃣ Uncertainties surrounding the Corebridge IPO. The market’s reception of Corebridge and AIG’s handling of its shares will have a material impact on stock performance. Since the IPO the share price has been relatively stable, but this may not continue, and it remains unclear how AIG intends to handle its 78% stake in Corebridge.

2️⃣ Uncertainties surrounding investments. Like most insurance companies, AIG holds a large and diversified investment portfolio. Market conditions and management decisions have an unpredictable impact on that portfolio’s value and returns, and on the value og the Company

3️⃣ Underwriting risk. One of the core challenges of P&C insurance is pricing policies at a level that is competitive enough to attract customers but high enough to cover any claims. A large concentration of claims from disasters or other events or a failure of underwriting and risk assessment could do significant damage to the Company’s financial standing.

Bottom line: AIG has fully emerged from its post-2008 near-collapse. The Company has sold off its less profitable units and is now fully focused on a highly profitable core business. Valuation ratios, margins, and returns are strong ans the company is arguable undervalued based on its past, not its present and future.

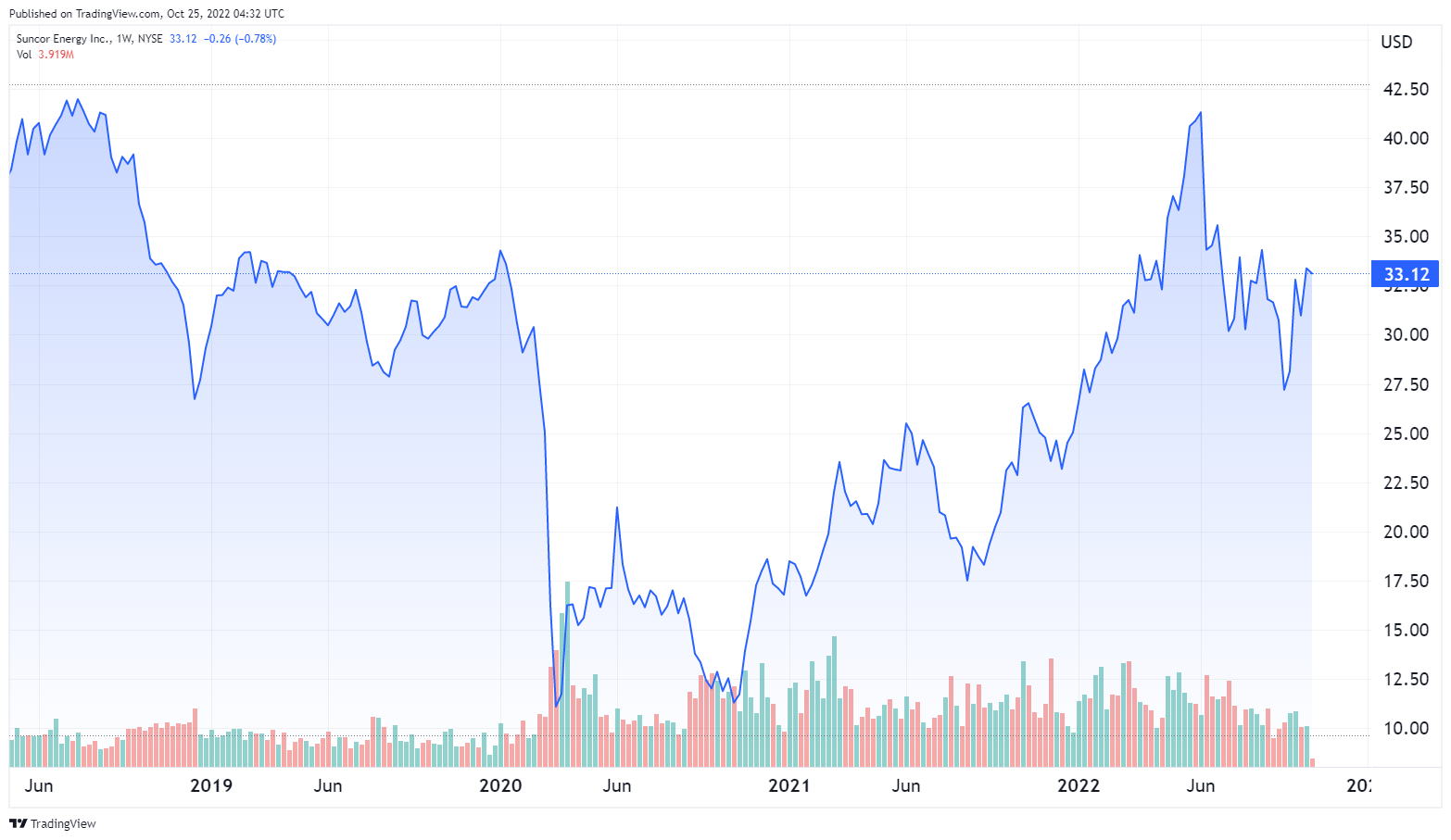

Suncor Energy Inc ($SU)

Source: tradingview.com

???? Summary:

- Share price at the time of writing: $

- Suncor is a Canadian oil company. Until recently it operated as a diversified energy company, but it recently sold its solar and wind assets.

- Suncor is Canada’s largest oil Company and specializes in the extraction, refining, and marketing of tar sands crude.

- $SU trades at a substantial discount to its industry peers. The dividend is high and the valuation ratios attractive.

???? What they do:

Suncor is a vertically integrated oil company engaged in production, transportation, refining, and distribution of hydrocarbons.

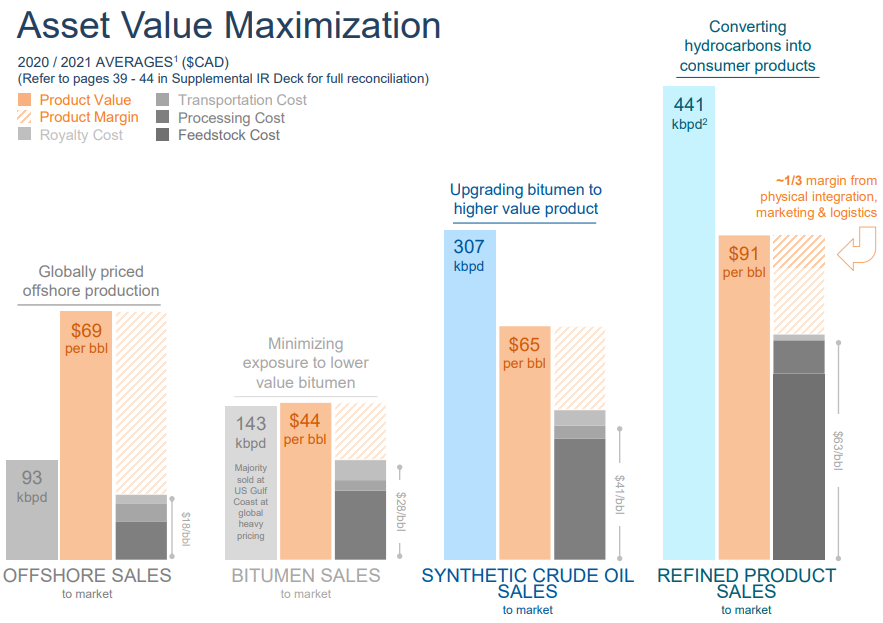

Suncor operates in four main divisions.

- Offshore (15% of AFFO*): Suncor produces high value crude in operations off Newfoundland, Scotland, and Norway, selling the output directly to the global market at Brent pricing.

- Base Energy Sources (10% of AFFO): unprocessed bitumen extracted from tar sands and sold at US Gulf Coast pricing.

- Synthetic Crude Oil (30% of AFFO): Synthetic crude is refined from bitumen at Suncor facilities, upgrading bitumen to a higher-value product.

- Refined Products: (45% of AFFO): refining hydrocarbons into consumer products for wholesale and retail marketing.

*AFFO = Adjusted Funds From Operations

This chart explains the Company’s integrated strategy:

Source: Suncor

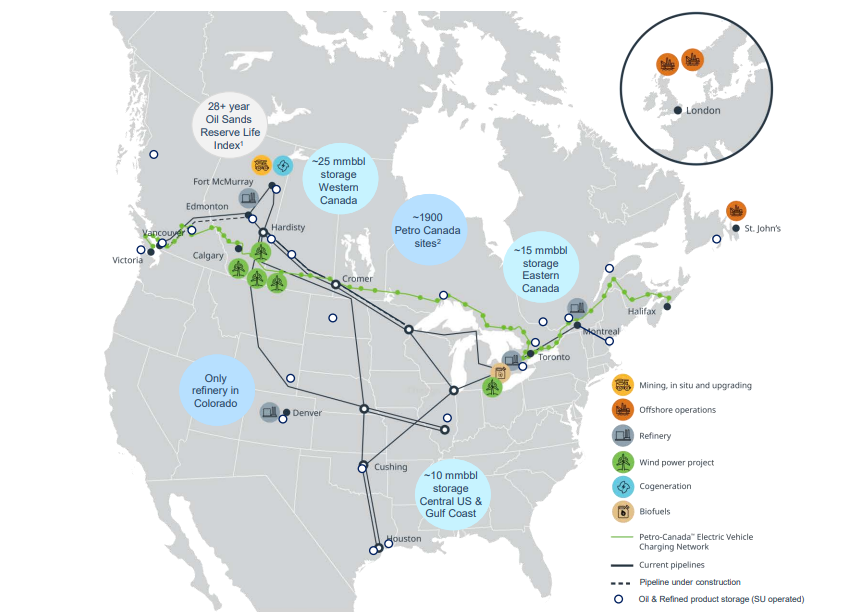

Suncor has production, refining, and distribution facilities across Canada and the US and in Europe.

Suncor has operated as a diversified energy company for many years. On Oct 5, 2022 Suncor announced the sale of its solar and wind assets to Canadian Utilities Ltd. for C$730 million. Suncor is now exclusively focused on oil, natural gas, biofuels, and hydrogen.

Suncor operates 1900 fueling stations under the Petro Canada brand, which provide both conventional fuels and electric charging stations. Petro Canada’s Electric Highway project provides EV charging stations at least every 250 km on a trans-Canada route.

Suncor is currently Canada’s leading producer of hydrogen.

???? What we learned from social media and institutional investment patterns:

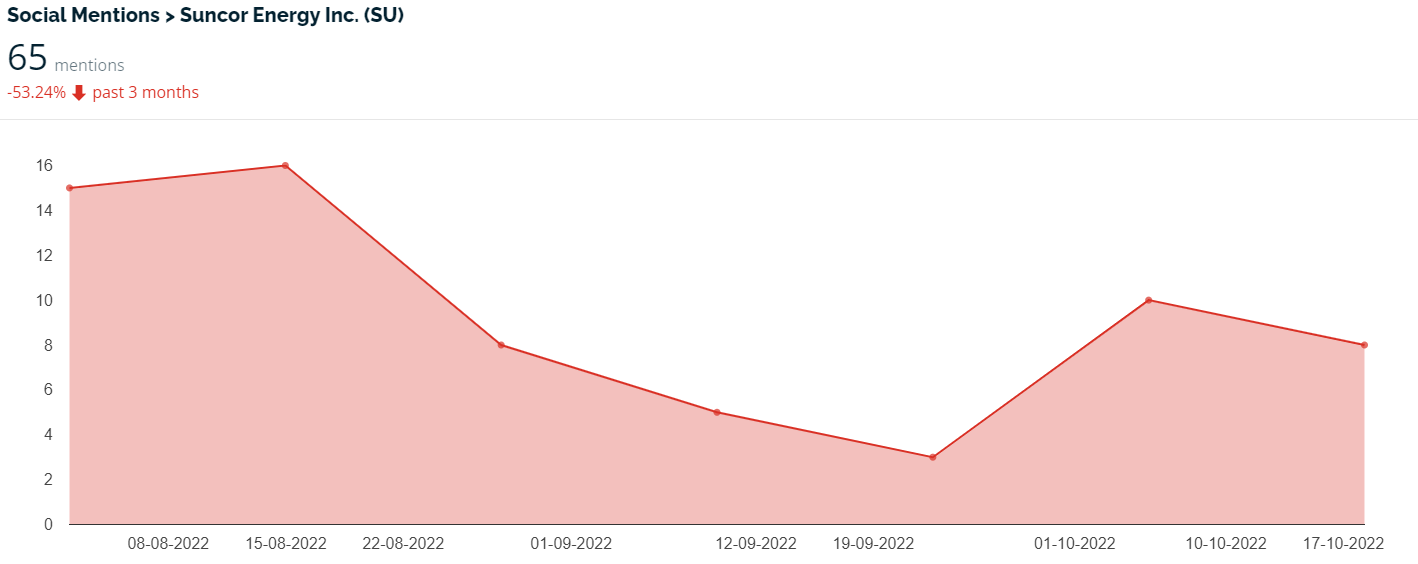

Suncor maintains a steady low level of social media attention:

Source: marketsentiment.com

Most of the discussion occurs on threads specific to Canadian stocks and Canadian energy stocks in particular. Overall, Suncor is being closely watched in a relatively small, specialized community and ignored in the wider retail investing community.

This is not surprising: many US investors simply don’t look at companies outside the country, and when they think of oil they focus on the US majors.

Institutional investment is a relatively low 65.35% of the Suncor float, with the Royal Bank of Canada the largest shareholder.

Notable comments from Reddit:

“Got in at 31 in January because I thought it had room to go. Then russia went nuts and it really took off. The only reason I'm not sweating the volatility is the breathing room I've got. It really seems like it should run up higher with the price of oil where its at. All that cash should mean more buybacks to top it off”

– Luddites_Unite

“SU is a buy right now ! Will oil go below 70? Will COVID in China last forever? Will people stop flying or driving like crazy this Summer? Will Russia all of the sudden be a NATO friend? Will OPEC start producing more oil? Will the US frackers build new infrastructure ? Will SU management get away with not responding to Elliot? If you answered NO to most questions it means SU has a LOT of upside! 60+ as a matter of fact.”

– Bsdave103

???? Smart Money Signal ???? US-based Elliott Management owns 3.4% of Suncor. Elliott is a noted activist investor, and is pressuring Suncor to add new directors and make management changes. The stock has jumped from $36 to $50 since the Elliott announcement.

???? Why $SU could be valuable:

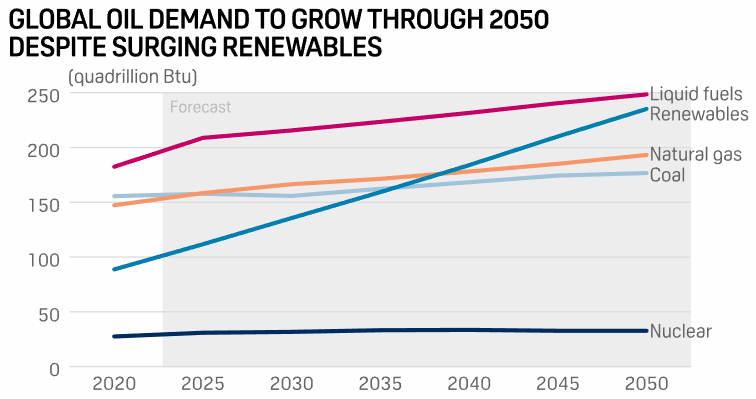

Oil prices are highly cyclical and very unpredictable in the short term. In the longer term, S&P Global Commodity Insights predicts a 47% rise in total energy demand through 2050, with oil still the leading energy source.

Source: S&P Global Commodity Insights

There’s no doubt that oil prices will fluctuate dramatically during this period, but steady demand and increasingly limited supply should sustain a fairly high overall pricing environment.

Rising production costs as “easy oil” is used up will exert upward pressure on prices: as prices fall below the break-even point producers will cut back, constraining supply and moving prices up.

Suncor’s long-term advantage in this mix is its location. Suncor’s operations are in politically stable environments with immediate proximity to major markets. Given the high level of geopolitical instability affecting major OPEC+ producers, this places Sucor in an ideal position to fill gaps when conflict, sanctions, or other issues interrupt supply in more sensitive producing areas.

Suncor’s refining capacity positions the company to take advantage of refinery capacity shortages in the US and Canada. Even if oil prices fall, refinery bottlenecks will support higher prices of finished products, and Suncor’s production capacity assures steady feedstock supply to its refineries.

Suncor stock is up 27% from a year ago, but the shares have dropped 26% from their August peak and they still lag behind the wider sector: the SPDR energy sector is up 43% This is despite exceptional performance: Suncor’s Q2 2022 earnings were up 360% and AFFO up 126% from the equivalent quarter last year.

Suncor as well as or better than more visible oil majors in many key metrics.

| ExxonMobil | Chevron | Suncor | |

| Revenue Growth* | 70% | 81% | 76% |

| Earnings Growth* | 280% | 277% | 360% |

| Free Cash Flow Growth* | 60% | 65% | 177% |

| Net Margin | 15.5% | 17.8% | 24% |

| Return on Equity | 23.05% | 20.24% | 24.68% |

* Most recent quarter, from equivalent quarter last year

Oil companies typically trade at low valuation ratios during periods of high oil prices, but Suncor’s ratios compare favorably.

| ExxonMobil | Chevron | Suncor | |

| Trailing P/E | 11.01 | 10.76 | 6.56 |

| Price/Sales | 1.23 | 1.52 | 1.17 |

Suncor has used its cash windfall in three major ways.

- Retiring debt. Like many energy companies, Suncor incurred substantial debt during the period of low oil prices. Debt is down 21% in the past 2 years.

- Share buybacks. Suncor has repurchased 88.2 million shares this year. Repurchases will probably accelerate if the stock price falls while income is still high.

- Dividends. Suncor pays a healthy 4.9% dividend with a highly sustainable 23.28% payout ratio.

The involvement of Elliott Management provides a continued external force pressing the company toward greater management effectiveness and encouraging necessary changes.

14 analysts currently cover Suncor. 2 rate it “Strong Buy”, 8 say “Buy”, and 4 say “Hold”. The average price target is $39.53, 25% above the current price.

Essentially Suncor is a play on oil prices. There are two prevailing themes regarding the overall direction of oil prices.

- Oil bulls believe that continued economic conflict with Russia, rising demand, and the determination of OPEC+ to support prices by cutting production will maintain a continued regime of above-average oil prices.

- Oil bears believe that a serious global recession will crush demand, OPEC+ nations will break discipline and pump more to support their budgets, and renewables will have a breakthrough, depressing oil prices.

If you’re in or near the oil bull camp, Suncor can be seen as a significant, if not global major, integrated oil company for sale at a desirable price. If you lean toward the bear side, you’ll want to avoid both Suncor and the entire sector.

⚠️ What the risks are:

1️⃣ Oil Prices. Both Suncor and the entire oil sector have benefitted from the recent oil prices surge. Oil prices are highly volatile and subject to speculative trading. An oil price collapse would have an immediate and major impact on Suncor.

2️⃣ Safety. Suncor has had 12 fatal accidents since 2014. Not all of the incidents can be attributed to the company – several were vehicle accidents and one involved a bear attack – but the company’s safety record and policies have come under scrutiny. The Company has pledged a safety review and policy changes, but more incidents could bring closer regulatory scrutiny and affect the Company’s public image.

3️⃣ Debt is a continuing concern. Suncor has retired significant amounts of debt, but it still owes over $17 billion, against 1.67 billion in total cash. As long as oil prices stay elevated this will not be a concern, but if prices crash again the company’s ability to raise further financing could be seriously impaired.

Bottom line: Suncor is essentially a play on oil prices. If oil prices stay high the sector overall will benefit. That expectation is already priced into the values of many oil majors, but less visible producers like Suncor have yet to see the benefit, and remain at attractive valuations.