Summary

Hubspot Inc provides Customer Relationship Management (CRM) software specifically designed for small and medium-sized businesses. It offers a highly rated product and consistent strong revenue growth, targeting a global market with enormous potential for expansion.

Paycom Inc supplies Human Capital Management (HCM) software focused on small to medium sized businesses. The Company is solidly profitable, revenues and earnings show consistent growth, and customer retention is strong. The stock is down 40% from its peak.

______________________________________________________________________

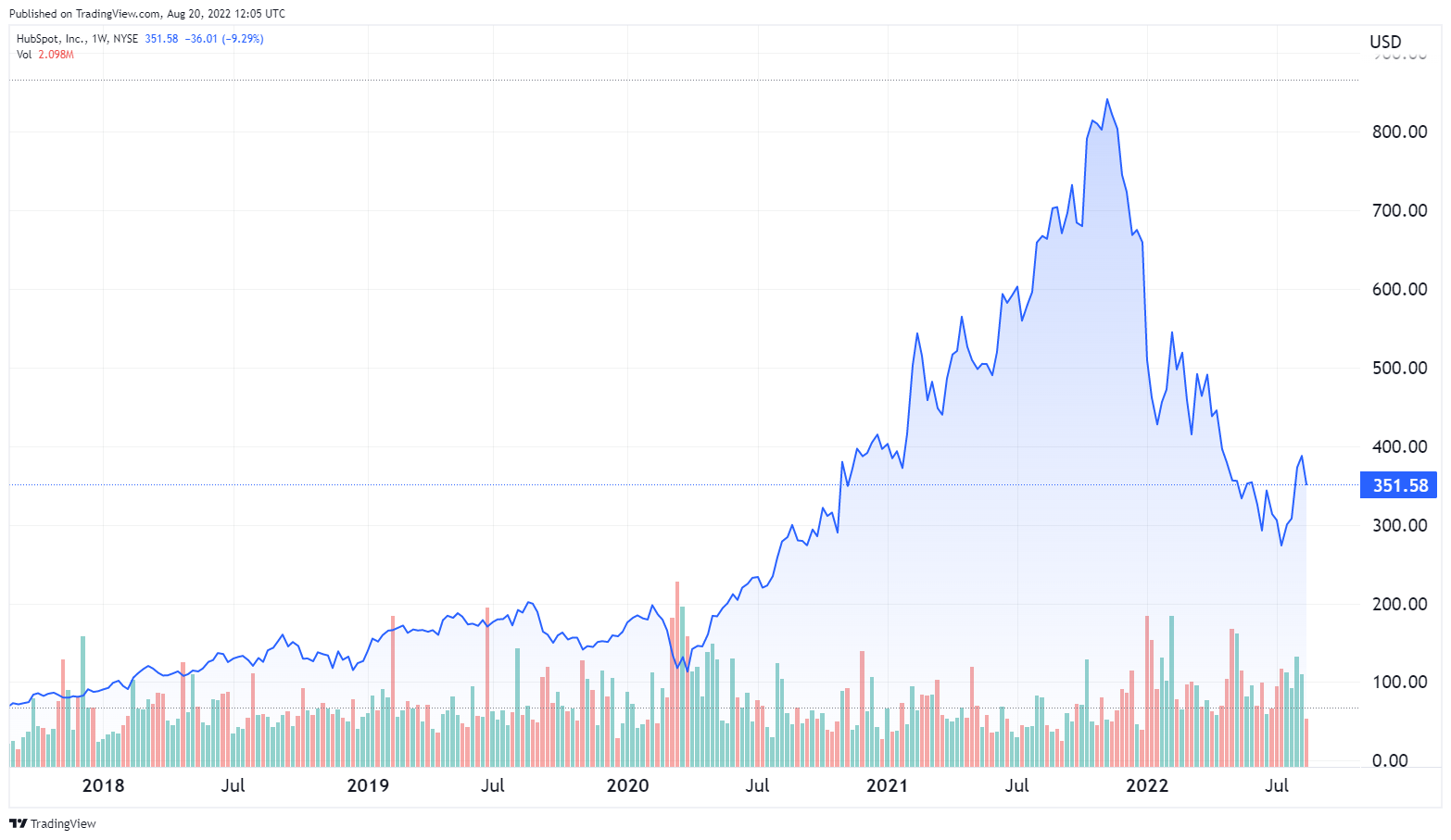

HubSpot Inc ($HUBS)

Source: tradingview.com

???? Summary:

- Share price at the time of writing: $351.58

- HubSpot had 150,865 customers at the end of Q2 2022, up from 135,442 at the end of 2021.

- Revenues grew rapidly in the first half of 2022 and the Company made significant R&D investments.

- $HUBS has a strong cash position that exceeds its debts by a significant margin.

- The share price is down almost 60% from its Nov. 2021 peak.

???? What they do:

Hubspot offers a subscription-based CRM platform oriented toward small to medium-sized companies. The Company has over 150,000 customers in over 120 countries.

At the end of 2021, over 50% of the Company’s customers were outside the United States. Non-US customers generated 46% of revenue.

The Hubspot CRM Platform offers a central database of lead and customer interactions and integrated applications designed to help businesses attract visitors to their websites, convert visitors into leads, close leads into customers, and transact with those customers.

The core CRM platform supports multiple hubs.

- The Marketing Hub helps marketers attract, engage, and nurture new leads through the entire customer lifecycle.

- The Sales Hub is designed to enhance the effectiveness and productivity of sales teams.

- The Service Hub helps businesses manage and connect with customers to develop positive customer service experiences.

- The Content Management System (CMS) Hub helps businesses generate new content tailored to specific customers, optimizing business websites to generate and convert leads.

All applications within the platform work through a single platform designed for growing companies. Companies can work with the applications they need and add others with minimal adjustment or disruption.

Hubspot offers an initial free product suite to build familiarity, after which customers can select additional products and services as they need them.

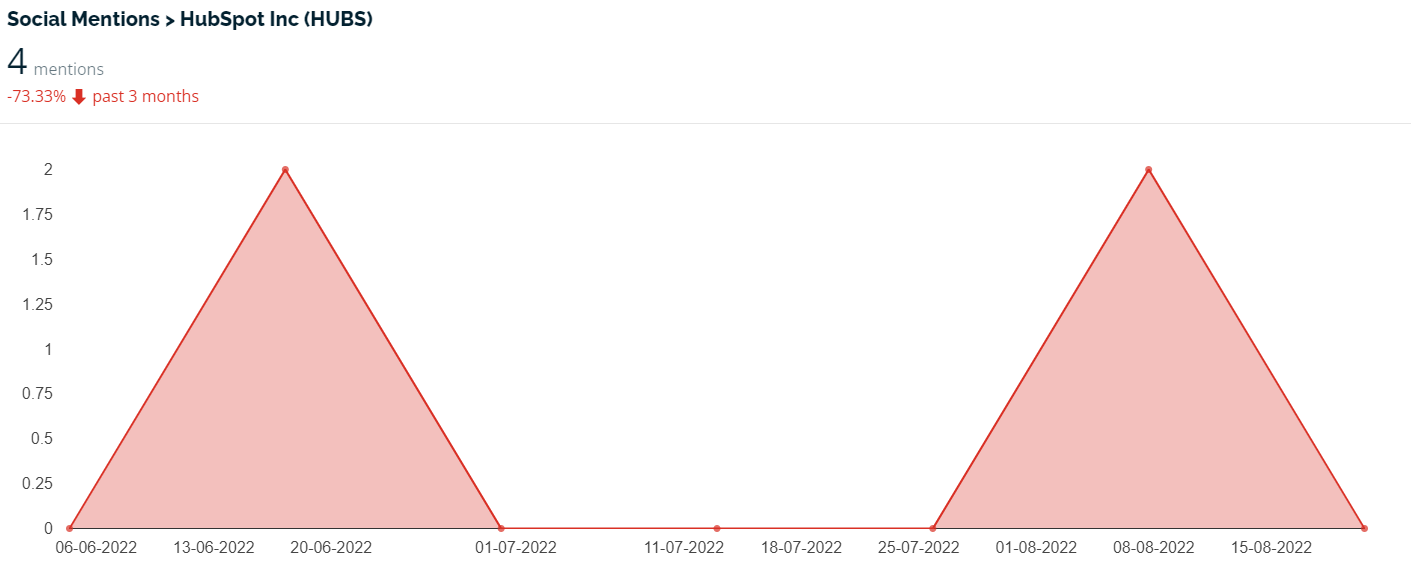

???? What we learned from social media and institutional investment patterns:

$HUBS has faded to virtual invisibility on social media, with only four mentions in the last three months.

That seems partly due to a comprehensive flight out of unprofitable growth-focused companies and partly because the Company markets its products almost exclusively to businesses. Few retail investors have any reason to be aware of Hubspot.

Looking farther back, we find more discussion in the past, fueled by exuberance during the stock’s rapid climb in 2020 and 2021 and misery during the plunge of 2022. The current silence suggests that most of the Reddit posters have given up on the stock.

Notable comments from Reddit:

“Most people I know in the sales leadership industry are starting to lean into Hubspot’s direction over Salesforce because the functionality and UI are just so nice and easy to work with. On top of that it’s effortlessly and endlessly customizable.”

– quiltedlegend

“HubSpot is primed to overtake Salesforce as an all in one platform for businesses to use for CRM, Marketing Automation, Service Desk software. It's so much cleaner and user intuitive. Ask any sales team and they will pick HubSpot over Salesforce any day. They are going to be HUGE, and super excited to watch them grow so strongly. This is a solid 5 to 10 years buy and hold.”

– applebologna

A massive 98.8% of the $HUBS float is owned by institutions, suggesting that retail investors have almost completely abandoned the stock. Holders are dominated by large institutions like T. Rowe Price, Vanguard, and Blackrock.

???? Smart Money Signal: Ken Griffin’s Citadel LLC bought 415,000 shares of $HUBS in the last 3 quarters, with 276,000 shares purchased in Q2 of 2022.

???? Why $HUBS could be valuable:

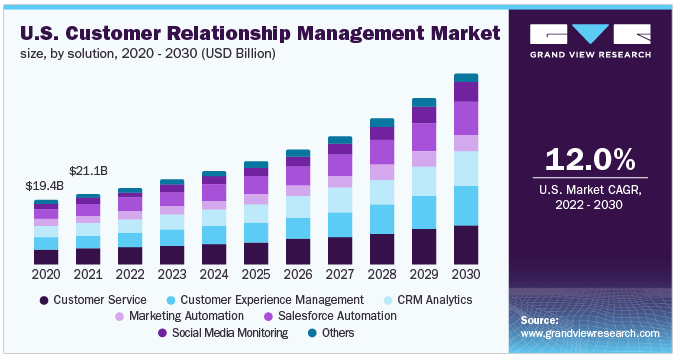

The global CRM software business is expected to grow at an exceptional CAGR of 13.3% through 2030.

The US market is expected to show a CAGR of 12% through 2030.

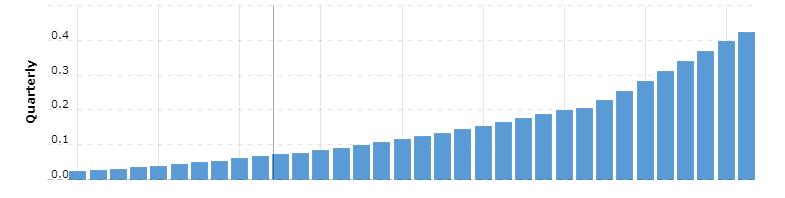

Hubspot revenues have increased steadily and consistently.

Source: Macrotrends

Gartner Peer Insights ranks HubSpot #1 among B2B Marketing Automation Platforms.

$HUBS is targeting an underserved niche with abundant room for growth. Much larger CRM companies (like Salesforce) dominate the large-company market, but smaller companies find their products overly complex and very expensive. Hubspot provides a package aimed at the needs of smaller companies and the “freemium” model lets companies that aren’t sure they need CRM software experiment without risk.

Most large companies have already adopted CRM software, which means that growth opportunity are limited to upselling current customers, poaching customers from other providers, or competing for the ever-dwindling pool of companies that have yet to select a platform. Small-to-medium sized companies have just begun migrating to CRM platforms, leaving far more room for growth.

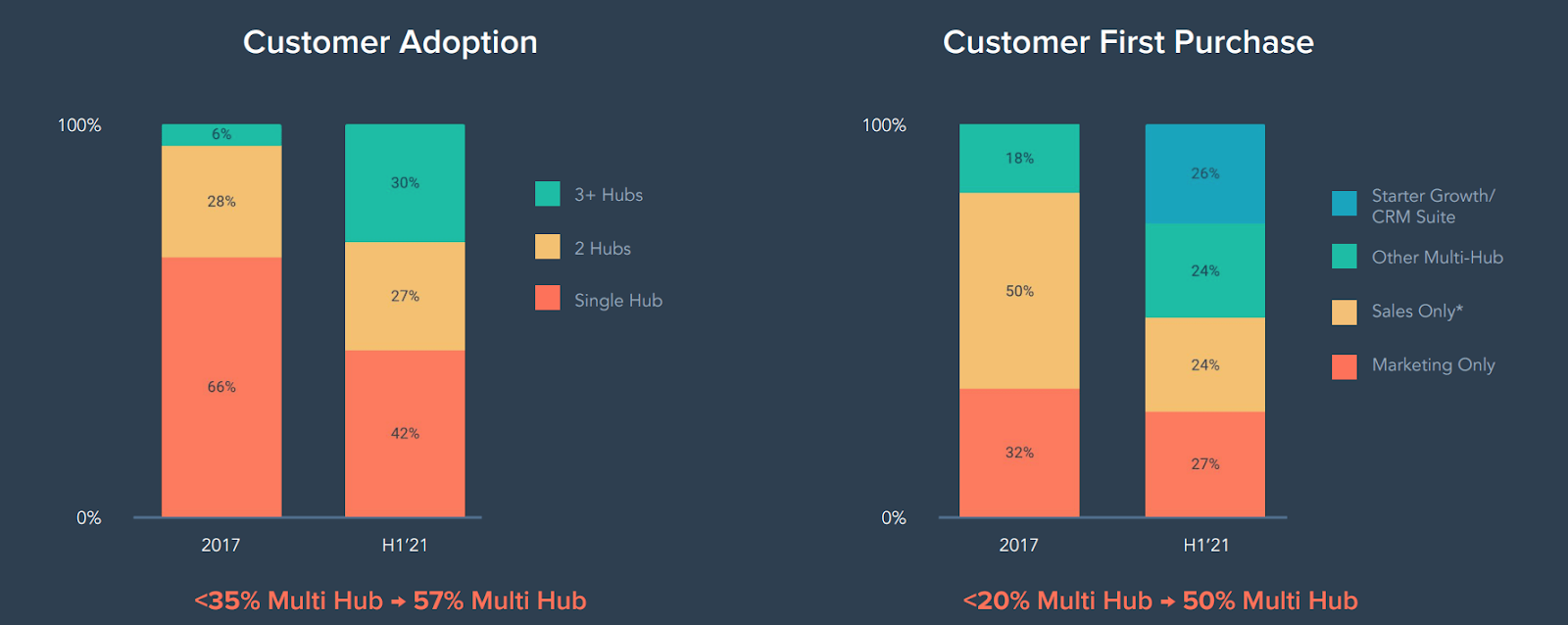

As Hubspot’s customer base has grown, customers have also moved toward adopting higher-value packages, even in their first purchase.

Source: Seeking Alpha

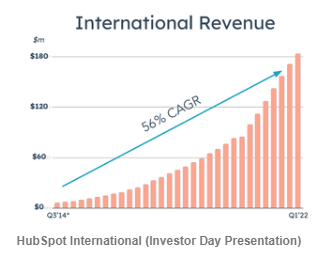

Hubspot’s international revenue has grown rapidly, indicating rising popularity among a huge potential customer base.

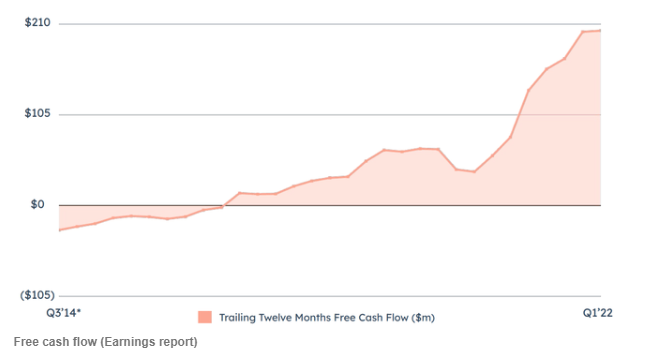

Free cash flow has grown dramatically.

Hubspot’s operating losses were $11.2 million in Q1 2022 and $56.4 million in Q2 2022. Against this we can offset a $326 million R&D expense over the last 12 months, suggesting that the Company is sacrificing immediate profitability to build long-term competitiveness and trim current tax liabilities. The gross margin is an exceptional 80%, suggesting a high potential for profitability.

$HUBS has a strong balance sheet with $1.2 billion in cash and under $750 million in debt, making the Company effectively debt-free.

20 analysts currently cover $HUBS. 7 rate it a Strong Buy, 9 say “Buy”, and 4 say “Hold”. The average price target is $437.12, 24% above current levels.

⚠️ What the risks are:

1️⃣ $HUBS operates in a highly competitive market. Major players like Salesforce and Adobe may introduce products aimed at Hubspot’s target niche, and existing competitors will expand their offerings. Hubspot will have to continuously innovate and improve to maintain and expand its market share.

2️⃣ The customer base is volatile. Small and medium-sized companies fail at a much greater rate than large, established companies. Hubspot may see customers drop out, particularly if the economy sinks into full recession.

3️⃣ Hubspot is not currently profitable and may not achieve profitability. The current market environment is not friendly to non-profitable companies and there is no way to know when this will change. Any adverse event or report may have exaggerated consequences for the stock price as long as the company is unprofitable.

Bottom line: $HUBS is a high-potential growth stock with a stock price that’s been heavily penalized simply because the market is in a cycle that’s unfavorable to growth stocks. It has a strong competitive position, a solid balance sheet, and steady growth, and is well positioned to benefit when the market cycles back to growth.

Paycom Software Inc ($PAYC)

Source: tradingview.com

???? Summary:

- Share price at the time of writing: $377.01

- Paycom Software Inc provides cloud-based Human Capital Management (HCM) software designed for small to medium-sized companies.

- Products are provided on a Software as a Service (SaaS) model, on a subscription basis.

- $PAYC is highly profitable, with strong revenue and earnings growth and no debt.

- Shares have dropped almost 40% from their October 2021 peak, reflecting an overall flight from growth stocks.

???? What they do:

Paycom provides a comprehensive cloud-based HCM solution targeting small and medium-sized companies. Paycom originally targeted companies with 50 to 2000 employees but has recently begun taking on clients with as many as 10,000 employees.

The platform manages the entire employment life cycle, from recruitment through retirement.

The platform uses a single database for multiple HCM functions, including:

- Talent acquisition: applicant tracking, candidate tracking, enhanced background checks, onboarding, electronic signature verification, and tax credit services.

- Time and labor management: time and attendance monitoring, scheduling and schedule exchange, time-off requests, Labor allocation, management reports, geofencing/geotracking, and microfencing.

- Payroll: payroll and tax management, expense management, mileage tracking, garnishment administration, and a payroll concierge service generating multiple reports and data maps.

- BETI: Paycom’s Better Employee Transaction Interface (BETI) is a proprietary system allowing direct employee input and checking on the payroll process, generating improved efficiency and error reduction.

- Talent management: employee self-service, compensation management, performance management, position management, analytics, and learning/content subscriptions.

- HR Management: remote management control, direct data exchange, employee question management, documents and checklists, compliance, benefits enrollment and administration,

Many organizations now use multiple unlinked services to provide these functions, limiting their capacity to control information and generate useful analytics.

The Paycom solution minimises the risk of compliance failures while maintaining data integrity to generate actionable analytics.

Paycom serves over 33,900 clients, with no single client accounting for more than 0.5% of revenues.

Payroll applications provide the majority of revenue, but Paycom does not track revenue across other applications because they are sold in different combinations.

???? What we learned from social media and institutional investment patterns:

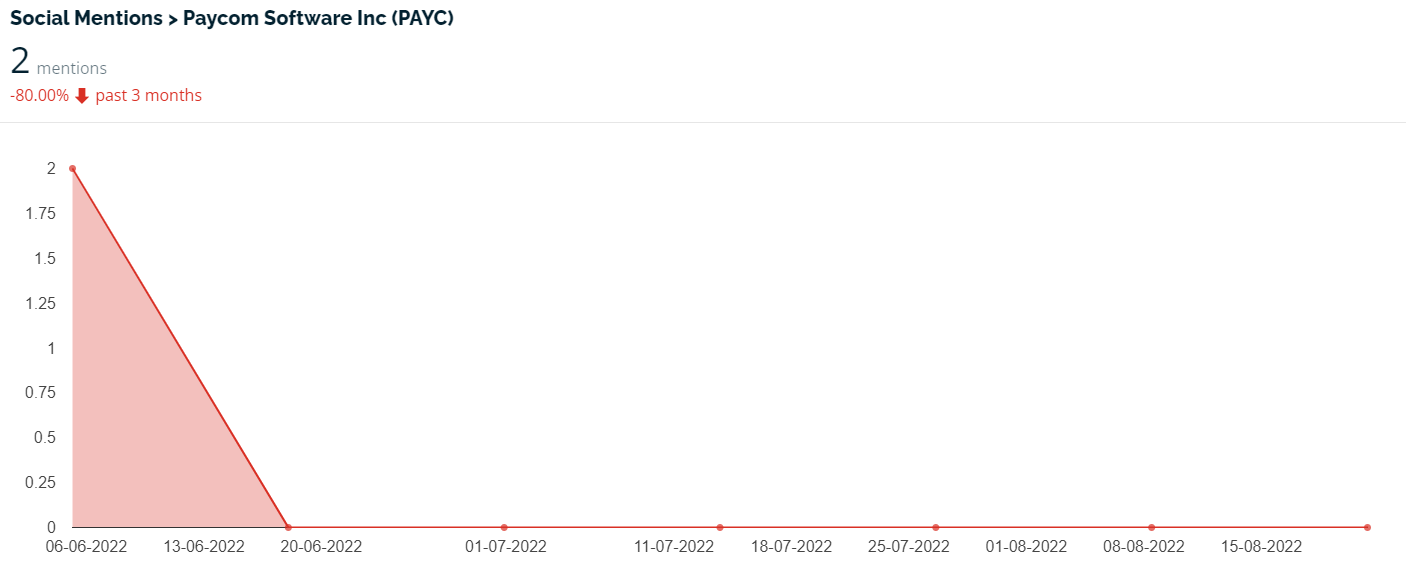

Paycom is virtually invisible on social media. Part of that is due to the flight from growth stocks and, like Hubspot, a product that is not familiar to most consumers. Even in the growth-focused days of 2020, though, there was littel discussion of Paycom, only occasional posts with little or no engagement.

There’s no clear indication of why Paycom failed to catch Reddit’s attention heaven when it was leaping from $165 per share in March 2020 to $547 per share in October 2021. Social media patterns don’t always have a clear explanation. It does seem safe to say that future movements will probably not be driven by social media attention.

An unusually large 15% of Paycom’s 60 million shares are held by insiders. Another 77% is held by institutions, with Blackrock and Vanguard the dominant holders.

???? Smart Money Signal ???? Ken Griffin of Citadel bought 331,000 shares of $PAYC in the 2nd quarter of 2022.

???? Why $PAYC could be valuable:

The global HCM software market is expected to show a CAGR of 9.6% through 2030.

Paycom is targeting small and medium sized companies that are not effectively served by the complex systems provided by major competitors. This niche also provides room for growth, as there’s limited penetration of modern full-service software suites.

Management estimates that Paycom has captured only 5% of its total addressable market.

Despite inflation and a general economic downturn, the US labor market continues to be robust. Unemployment is below 4% and the economy is adding jobs at a solid pace. In that environment businesses have a strong incentive to optimize recruitment and management of employees.

Paycom’s unique BETI interface allows employees to review and approve their paychecks before submission, dramatically reducing payroll disputes.

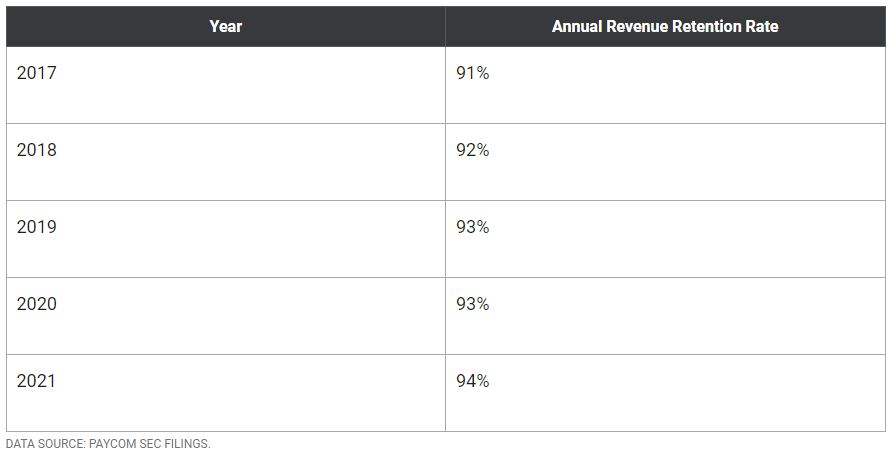

Paycom’s annual revenue retention rate – a crucial measure of customer satisfaction – is high and has improved consistently year over year.

Revenue growth, earnings growth, and free cash flow growth are all well above median levels for the sector.

$PAYC has committed $1.1 billion through 2024 to a share repurchase program aimed at building shareholder value.

Q1 revenue was up 29.9% over the equivalent quarter last year, and Q2 revenues jumped 31%.

Paycom has a strong balance sheet, with over $279 million in cash and only $29 million in debt. Aside from the lack of debt, Paycom holds client payroll funds and earns interest on them. That combination means the Company should suffer little or no direct adverse impact from rate hikes.

Paycom’s combination of growth, profitability, high margins, low debt, and strong cash flow is unmatched among immediate competitors.

16 analysts currently cover Paycom. Nine rate it “Strong Buy”. Two say “Buy”, and four say “Hold”.

⚠️ What the risks are:

1️⃣ Paycom’s revenue growth is being driven to some extent by the growing labor market (Paycom bills on a per-employee basis). If the economy sinks into recession and the labor market swings toward higher unemployment, results could be affected.

2️⃣ Paycom’s valuation ratios are high. Even after its recent decline the stock trades at over 100x trailing earnings and over 19x sales. If the growth rate declines at all the valuation could become a major issue for current holders.

3️⃣ $PAYC operates in a highly competitive market, with competition from both agile startups and larger companies. Failure to continuously improve and upgrade the product could result in rapid erosion of the Companhy’s competitive position.

Bottom line: Paycom is a stable, solidly profitable, fast growing player in a rapidly growing industry. This is a growth play and the valuation will be an issue for investors with a low risk tolerance or a short time horizon, but the Company is well positioned to benefit from the strong labor market and a potential cyclic recovery of growth stocks.