Summary

Global Payments Inc provides payment processing solutions to businesses worldwide. The company has seen its share prices plunge despite continuous increases in revenue and earnings, and is well-positioned to gain from the global explosion in e-commerce and remote payments.

Markel Industries is the world’s largest manufacturer of medical devices, with a huge product portfolio spanning several major sectors. It’s a solidly profitable dividend aristocrat that dominates a recession-resistant business with long-term growth potential.

______________________________________________________________________

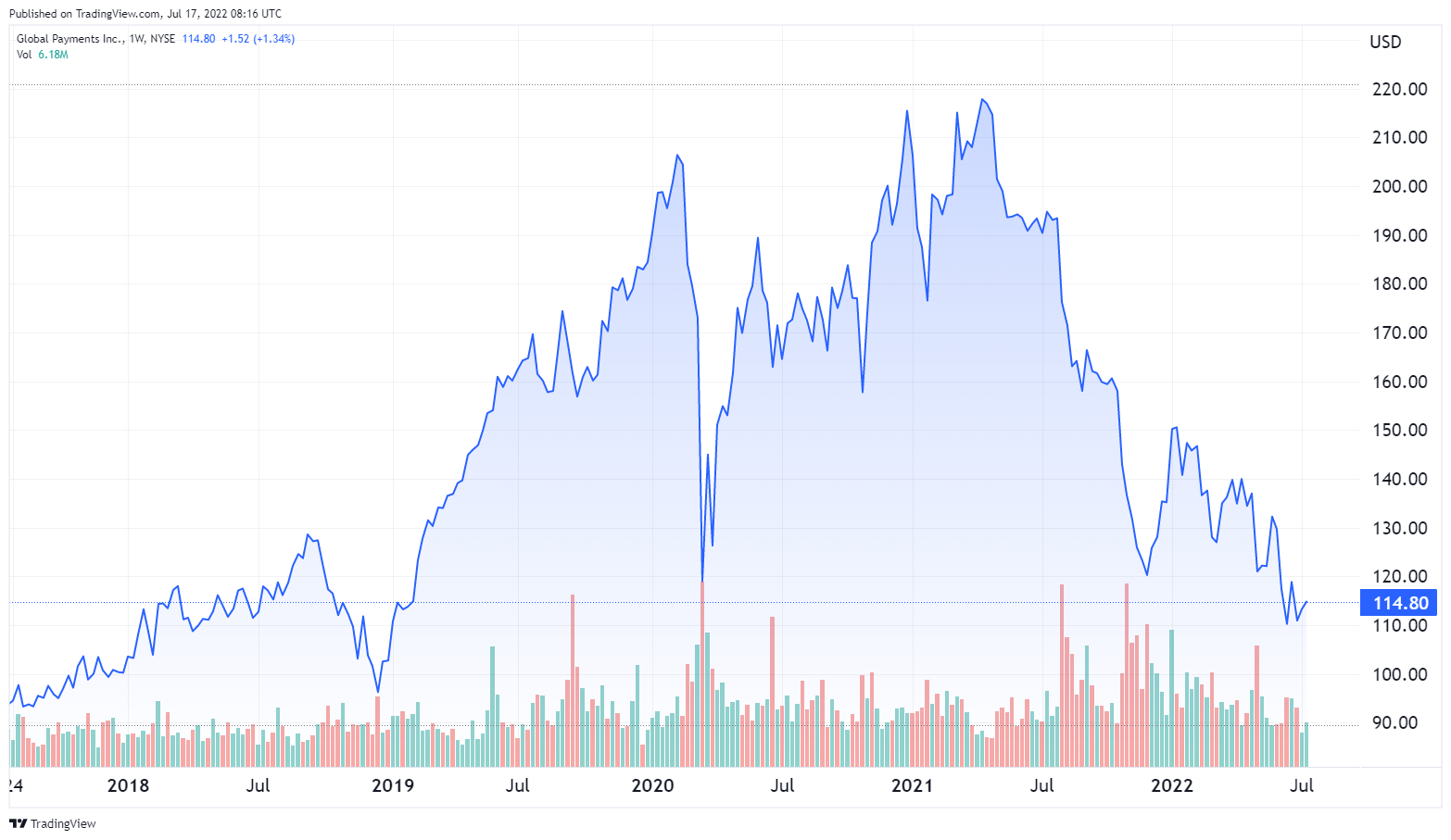

Global Payments Inc ($GPN)

Source: tradingview.com

???? Summary:

- Share price at the time of writing: $114.80

- Global Payments Inc is a payment processing company providing solutions to businesses worldwide.

- $GPN currently serves 4 million merchant locations and 1350 financial institutions in over 170 countries.

- The share price is down almost 50% from its April 2021 high despite consistent revenue and earnings increases.

- Valuation ratios are very reasonable considering the company’s rapid growth and strong competitive position.

???? What they do:

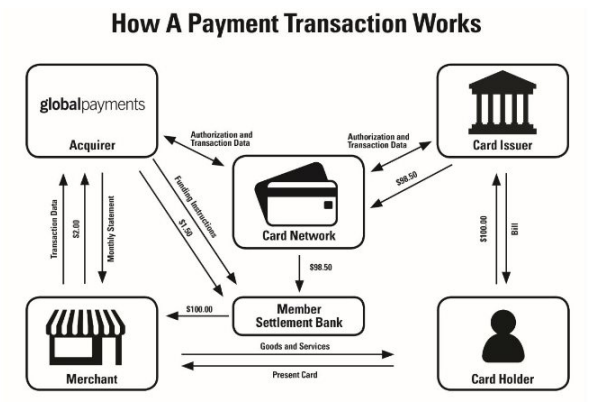

Global Payments Inc provides software and payment technology solutions for electronic, card, digital, and check-based payments. The Company operates in 170 countries in North and South America, Asia-Pacific, and Europe.

Global Payments operates in three business segments.

Merchant Solutions offers authorization, settlement, and funding services, customer support and help desk functions, terminal rental, chargeback solutions, payment security, sales and deployments, billing and statements, and online reporting.

The Merchant Solutions segment also offers enterprise software, point, of sale solutions, analytic tools, and human capital management solutions, all designed to help customers streamline operations and maximize efficiency.

Issuer Solutions offers a comprehensive card management platform for financial institutions and retailers. They also provide commercial payment and electronic payments solutions for businesses and governments.

Business and Consumer Solutions provides reloadable prepaid debit and payroll cards, demand deposit accounts, and other consumer-focused solutions.

In the most recent quarter the Merchant Solutions segment provided 68.3% of revenue, Issuer Solutions brought in 23.7%, and Business and Consumer Solutions provided 9%.

Global Payments does not have to manage payment risk for credit-based solutions, as it provides only the technology platform.

Source: Global Payments

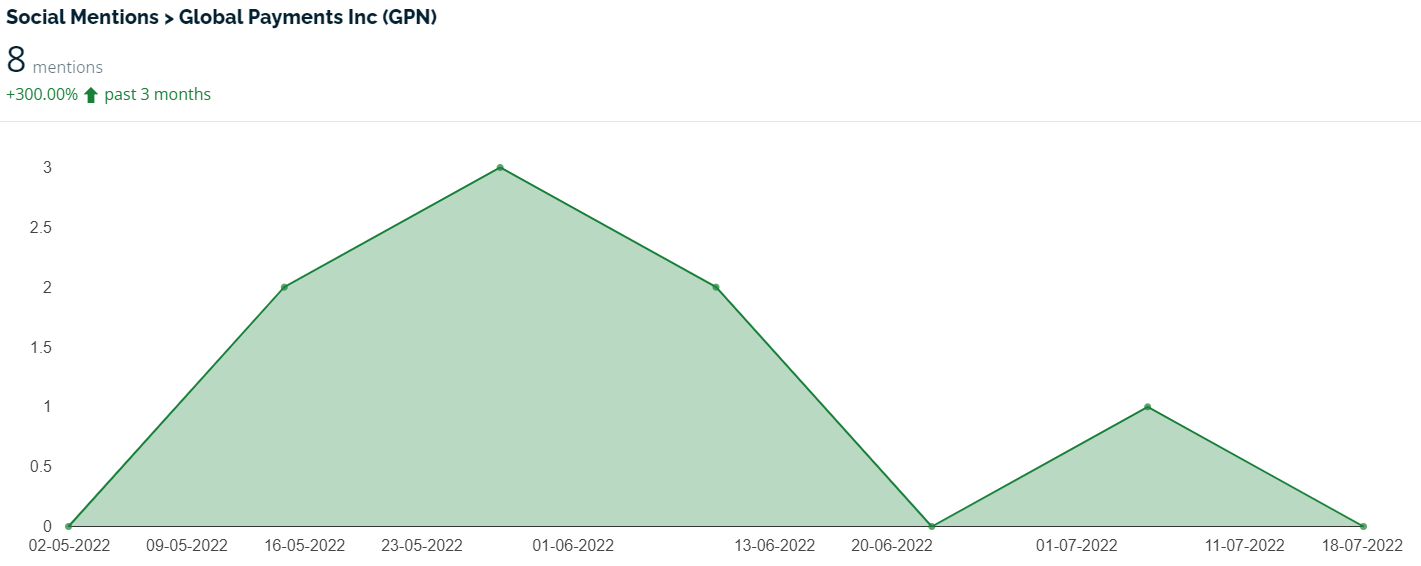

???? What we learned from social media and institutional investment patterns:

$GPN is the opposite of a meme stock. Almost every American has used its services, but almost nobody has heard its name. Even though the Company is ubiquitous in its space, it remains under the radar because it does not sell its products and services to consumers.

That anonymity has carried over to retail investors, with social media mentions peaking at three after the release of its last quarterly report. You have to go back to 2020/2021, when the stock was soaring, to find any significant social media discussion.

It’s no surprise to see stock ownership concentrated among institutional holders, with 88% of the float held by institutions led by the usual suspects: Vanguard, Blackrock, Wellington Management, and T. Rowe Price.

???? Smart Money Signal: Ray Dalio purchased 71,000 shares of $GPN in the last three quarters. Michael Burry opened a position with a 67.000-share purchase in the first quarter of 2022.

???? Why $GPN could be valuable:

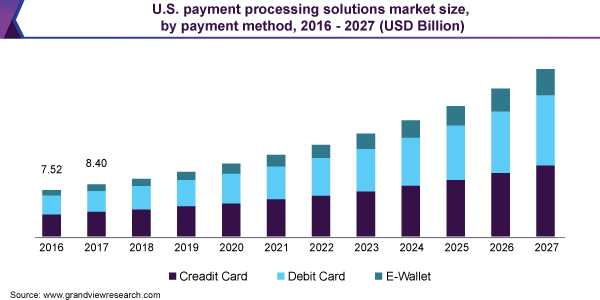

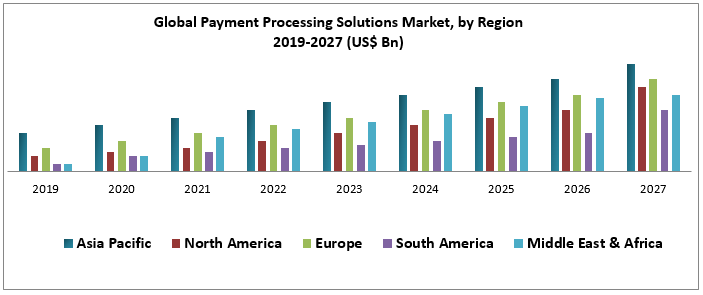

The global payment processing business is expected to grow at an exceptional CAGR of 14.5% through 2027.

The US market is expected to show particularly strong growth.

Source: Grandview Research

The Asia-Pacific region, where huge populations are moving rapidly toward e-commerce and remorse payment solutions, is also a leading market:

Source: Maximize Market Research

Global Payments is an established, highly competitive firm with a global footprint and an unequaled range of services, and is ideally positioned to benefit from the rapid expansion of e-commerce and online payments worldwide.

$GPN has displayed exceptional revenue growth in recent years, establishing a pattern that you’d expect to see in an early-stage startup, not a dominant industry player:

Source: Yahoo! Finance

$GPN is forecasting a 9% to 10% increase in revenue and a 16% to 19% increase in EPS for 2022, despite a general economic slowdown.

$GPN had an exceptional 1st quarter in 2022, demonstrating that it’s capable of delivering solid results even during periods of economic instability.

$GPN is trading at 12x forward earnings and 3.83x sales, a very reasonable valuation given the Company’s growth rate. The Price/Earnings Growth (PEG) ratio is a very attractive 0.71.

Global Payments has beaten analyst consensus earnings estimates for 4 consecutive quarters.

34 analysts are currently covering $GPN, with 11 rating it a “Strong Buy” and another 15 saying “Buy”. The average price target is $71.66, 49.5% above the current stock price.

⚠️ What the risks are:

1️⃣ $GPN faces extraordinary cybersecurity challenges. Global Payments handles enormous amounts of confidential personal and transaction data. Any security breach could involve significant liabilities and potentially irreparable damage to the Company’s reputation.

2️⃣ Acquisitions may not be advantageous. Global Payments made several significant acquisitions in 2021. These and future acquisitions could incur share dilution or increased debt. If the Company fails to effectively integrate these acquisitions they could have a negative impact on results.

3️⃣ Competition is intense. The Fintech business is competitive and dynamic, with large numbers of new players offering disruptive technologies and major competitors offering analogous products and services. If Global Payments falls behind in the technology race it could rapidly lose market share.

Bottom line: $GPN is a highly competitive global player in a fast-growing industry with almost unlimited potential. Revenue growth is strong, valuation is reasonable, and after a 50% decline from the peak stock price, a recession appears to be already priced in.

Medtronic Plc ($MDT)

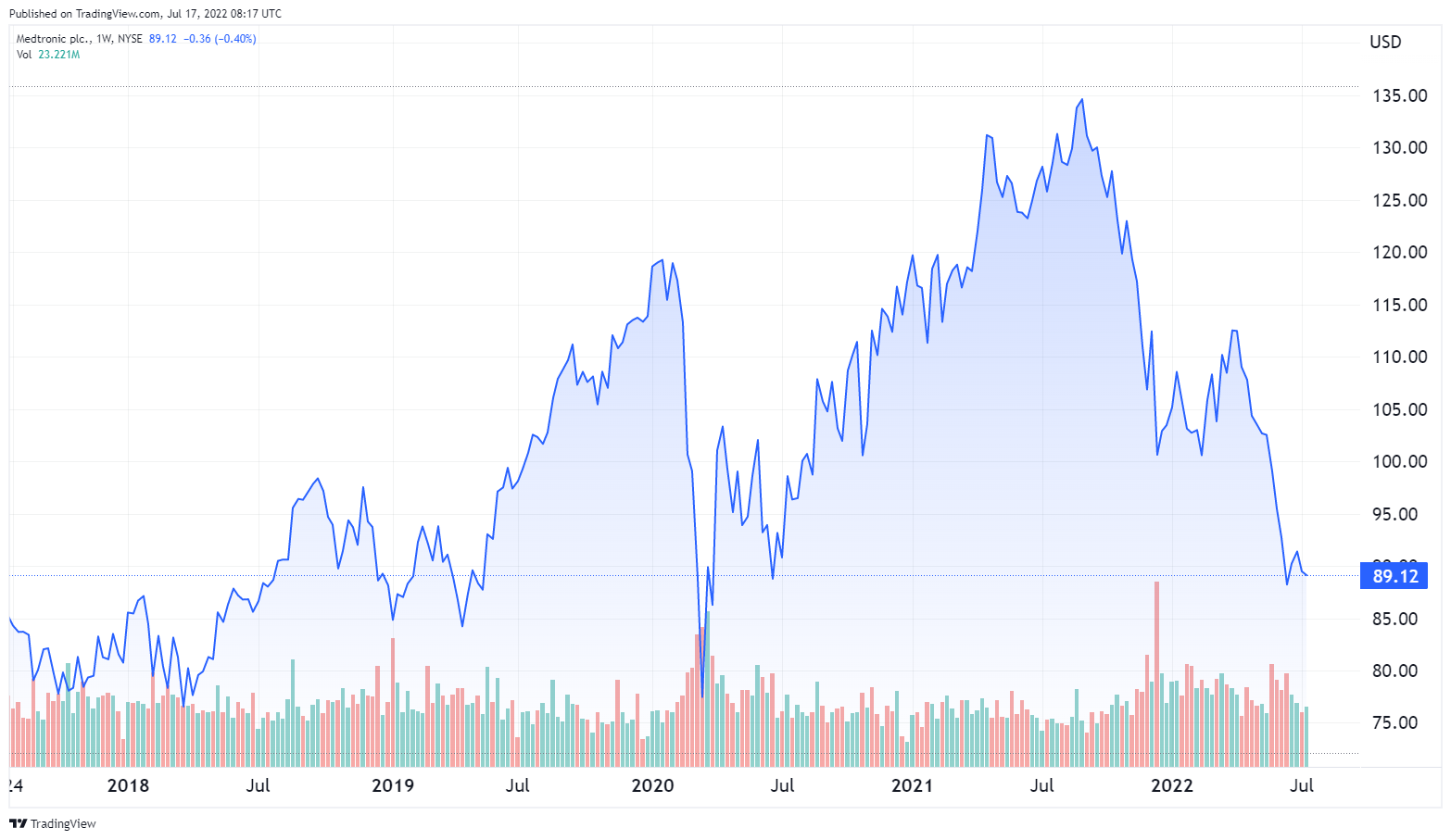

Source: tradingview.com

???? Summary:

- Share price at the time of writing: $89.12

- Medtronic Plc develops, manufactures, and sells device-based medical therapies and services.

- Medtronic calls itself “the leading global healthcare technology company”. It operates in over 150 countries and holds over 49,000 patents.

- $MDT is a highly stable company, paying solid dividends and dominating a growing recession-resistant business.

- Shares have dropped almost 34% from their August 2021 peak, boosting dividend yield and producing attractive valuation ratios.

???? What they do:

Medtronic was founded in 1949. In 2014 the Company acquired Covidien, an Irish manufacturer of devices for minimally invasive surgery. The deal nearly doubled Medtronic’s sales. Medtronic moved its corporate headquarters to Dublin at the same time, gaining tax advantages.

Medtronic currently operates worldwide in four operating and reportable segments. Each of these segments produces and sells dozens of products, far too many to discuss here. We’ll give a review with some examples.

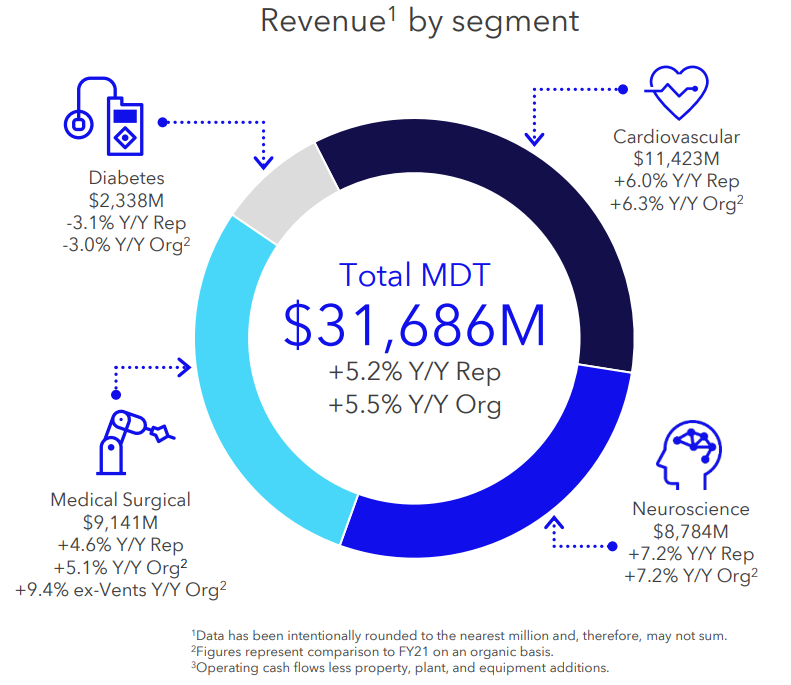

- The Cardiovascular portfolio provides products including implantable cardiac pacemakers, implantable cardioverter defibrillators, aortic valves, surgical valve replacements, stents, angioplasty balloons, and many others.

- The Medical Surgical Portfolio includes products like advanced stapling and energy products, electrosurgical hardware and instruments, robotic and digital surgery technologies, endoscopy products, hernia repair products, and numerous others.

- The Neuroscience Portfolio includes advanced neurosurgery products, products to treat degenerative disc disease, spine tumors, and other spinal conditions, titanium interbody implants, artificial discs, synthetic bone graft products, and more.

- The Diabetes Operating Unit provides insulin pumps and consumables, continuous glucose monitoring systems, smart insulin pens, and other products for managing and treating diabetes.

Medtronic announced in June 2022 that it has had over 200 product approvals in the last 12 months. The Company has over 230 ongoing clinical trials in 2022.

Medtronic produces industry-leading products with a reputation for state of the art innovation and quality. The Company spent $2.7 billion on R&D in its last fiscal year to maintain that position.

???? What we learned from social media and institutional investment patterns:

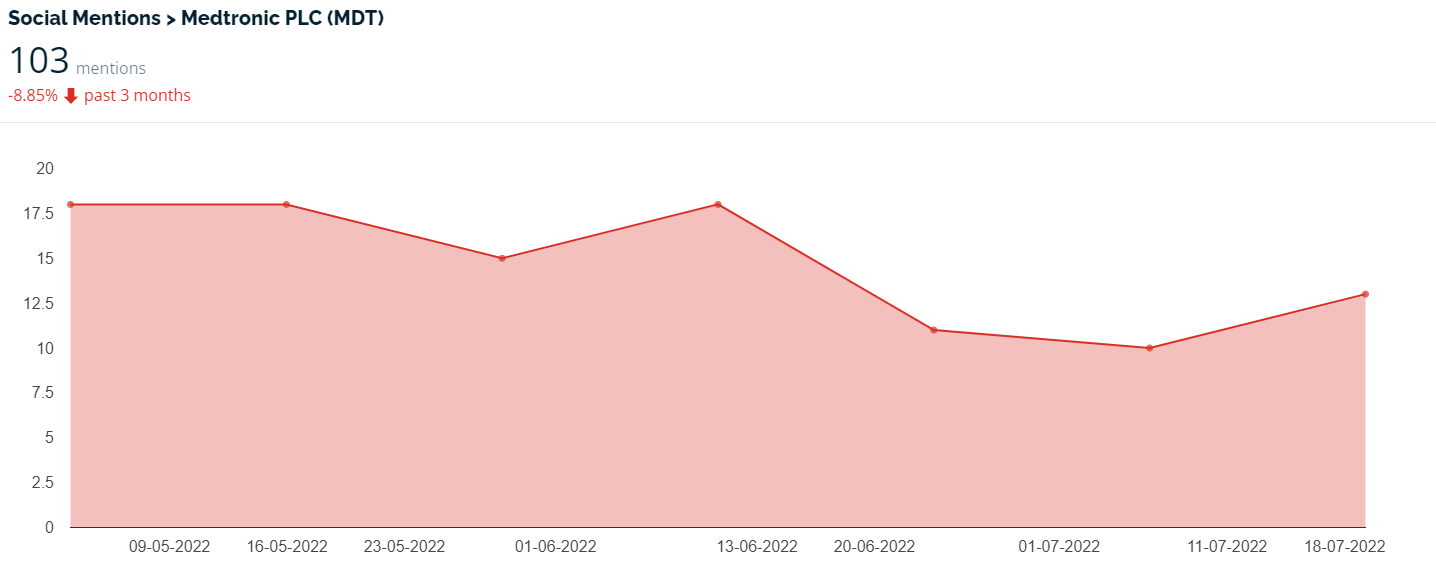

Medtronic maintains a steady level of social media discussion. This does not indicate that the stock is on the “viral” level or anything close to it.

Most of the mentions are on threads discussing dividend-bearing stocks, which typically attract discussion and attention during market downturns. Medtronic has increased its dividend every year for 45 consecutive years, placing it firmly in the “dividend aristocrat” category and pushing up toward the “dividend kings” that have increased dividends every year for 50 consecutive years.

The $MDT social media profile seems driven more by interest in dividend-bearing stocks in general than in the Company itself.

84.32% of the $MDT float is held by institutions, a relatively typical level. Holdings are dominated by industry giants Blackrock and Vanguard, again a fairly typical ownership profile.

???? Smart Money Signal ???? Ray Dalio bought 2 million $MDT shares in the first quarter of 2022. Kenneth Fisher of Fisher Investments has bought shares in every quarter for nine consecutive quarters, and holds a total of 2.77 million shares.

???? Why $MDT could be valuable:

The medical devices market is expected to show a CAGR of 5.5% through 2029.

Medical devices are not discretionary purchases. The market is thus highly recession-resistant. People get sick in all economic conditions.

Market growth is driven by secular trends: aging populations in the developed world and rising prosperity with increased demand for sophisticated medical services in developing economies.

Medtronic is the largest medical device maker in the world and dominates the market. Its products are used in hospitals all over the world. That size provides economies of scale and supports the intensive R&D spending needed to keep up in a rapidly evolving marketplace.

Medtronic has a continuing stream of new products coming into the market, driven by industry-leading R&D spending.

$MDT’s growth was significantly constrained by the COVID-19 pandemic. The Company devoted significant resources to boost the manufacture of respirators, and many procedures requiring higher-margin products were postponed, trimming demand.

Medtronic also shared the full design specifications and code for its industry-leading PB560 portable ventilator for free, allowing competitors to duplicate the unit to address the pandemic-driven ventilator shortage.

$MDT revenues have recovered to pre-pandemic levels, but growth has been constrained by significant supply chain issues, which have constrained manufacturing capacity.

The combination of pandemic impact and post-pandemic supply chain issues have created the impression that $MDT is a low-growth or no-growth stock attractive only for its dividend yield. It’s important to note that the constraints on $MDT have also applied to the industry as a whole and that $MDT has come through this difficult period retaining strong profitability and solid margins.

With the pandemic past and supply chain issues resolving, it is reasonable to expect growth in line with the overall industry anticipated growth rate. It is even possible (though not certain) that there will be a growth push as manufacturing capacity expands to meet pent-up demand.

$MDT trades at 15.92x forward earnings and 3.8x sales. Given the relatively stagnant growth rate over the last 3 years that might be considered high, but for a highly resilient dividend aristocrat with solid expansion potential it is reasonable.

The stock is trading near a 52-week low after a 34% decline, a potentially attractive entry point.

23 analysts cover Medtronic, with a consensus rating between “Buy” and “Hold” and an average price target of $112.62, almost 25% above the current level.

⚠️ What the risks are:

1️⃣ $MDT has experienced significant impacts from both the COVID-19 pandemic and the subsequent disruption of global supply chains. If COVID resurges or supply chain disruptions do not continue their current generally improving trend, results could be disrupted.

2️⃣ Medtronic operates in a highly regulated marketplace. Products must be approved by multiple and often divergent regulatory regimes in order to achieve global distribution and full sales potential. Failure to achieve regulatory acceptance for new products could affect results.

3️⃣ Medtronic’s products are used in critical applications and often make the difference between life and death. Any product failure, product recall, or another issue with performance or quality could have a huge impact on the Company’s reputation and viability.

Bottom line: Medtronic is a highly stable, resilient, blue-chip firm that dominates a growing, recession-resistant sector. It will never be a “growth stock” but it has solid potential to emerge from a recent period of stagnant growth. The stock is currently trading near a 52-week low at reasonable valuations.