ZIM Integrated Shipping Services Ltd is a veteran shipping company that’s only been public for a year, racking up impressive earnings and applying modern technology to bring customer service to a new level.

Franchise Group Inc is acquiring a portfolio of existing retail brands and using a franchise model to expand their store counts without taking on excessive debt. Earnings growth is rapid and management has a clear, focused business philosophy.

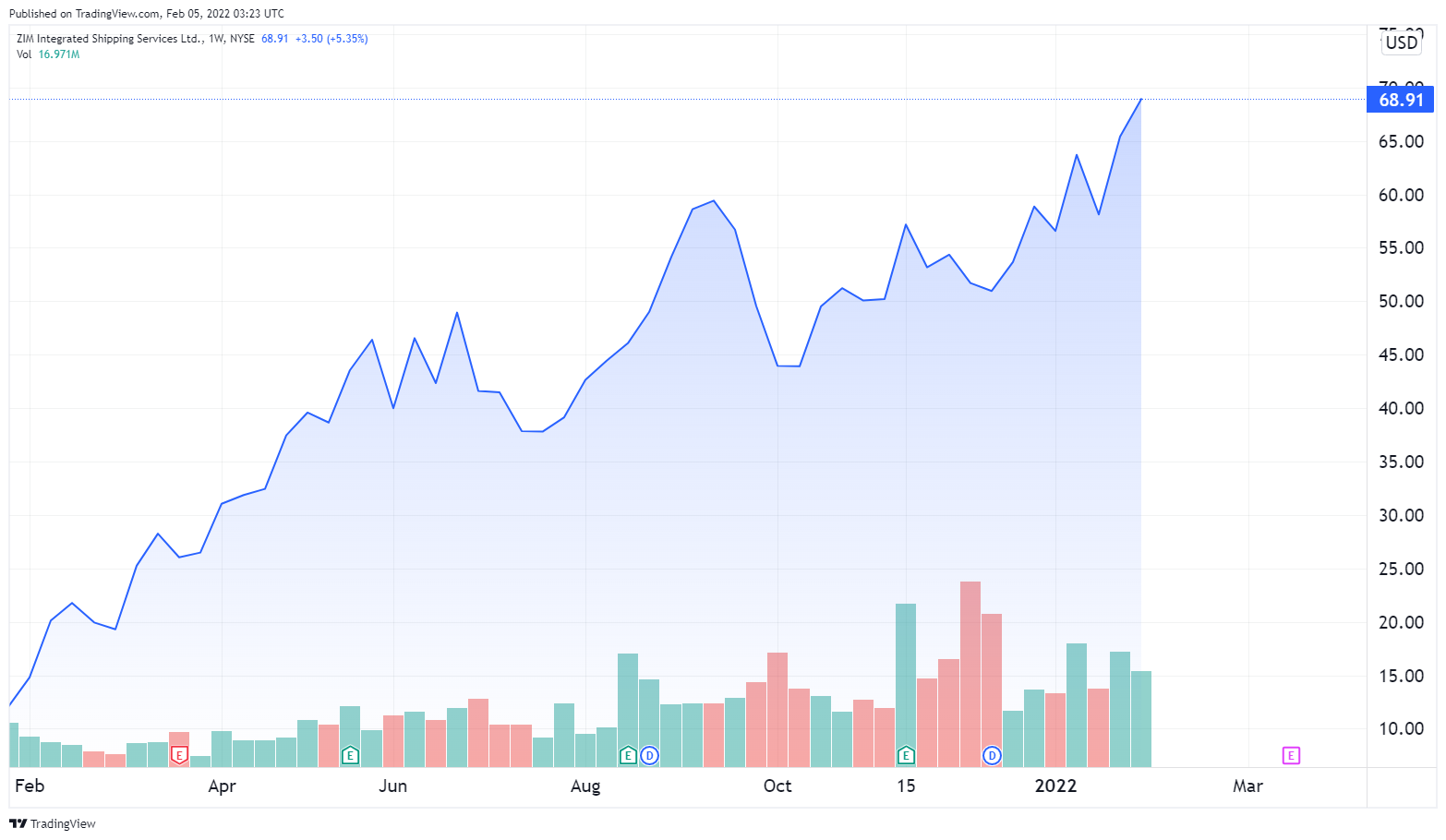

ZIM Integrated Shipping Services Ltd. ($ZIM)

Source: tradingview.com

Summary:

- Share price at the time of writing: $69.86

- $ZIM is a global container shipping and logistics provider headquartered in Israel.

- $ZIM operates worldwide but focuses on markets and routes where it holds a competitive advantage.

- Revenues and earnings have shown consistent increases and margins are excellent.

- $ZIM stock has soared since a relatively weak Jan. 2021 IPO, but still trades at only 0.94x sales and has a trailing P/E of 2.47

What they do:

ZIM Integrated Shipping Services Ltd is a global container shipping line based in Israel. The Company was founded in 1945 and has over 75 years of experience. ZIM uses an asset-light model relying primarily on chartered-in vessels rather than owned vessels.

ZIM operates a modern, specialized container fleet. As of March 31, 2021, the Company operated 101 vessels on 69 weekly lines across five geographic trade zones.

- Transpacific (41% of cargo)

- Atlantic (17%)

- Cross Suez (10%)

- Intra-Asia (26%)

- Latin America (6%)

ZIM provides value-added logistics services through subsidiaries in China, Vietnam, Canada, Brazil, India, and Singapore. These services include land transportation customs brokerage, and air freight, among others.

ZIM relies on cutting-edge technology to maintain an extremely high capacity utilization rate and operating efficiency. Customers can book shipments, calculate freight rates and other charges, request quotes, track shipments, trace container status, upload declarations, submit weight inquiries, and even estimate shipment-specific pollutant emissions on the Company website.

ZIM has an ongoing agreement with Chinese e-commerce giant Alibaba, which allows Alibaba buyers and sellers to purchase sea freight and logistics services from ZIM directly from Alibaba’s website.

What we learned from social media patterns:

Shipping is not a sector that typically generates heavy social media buzz, but $ZIM has seen substantial discussion over the last three months.

The November peak coincides with the release of Q3 earnings on Nov. 17. The report contained a remarkable set of numbers and drove a surge in the discussion, but even as that surge wore off the stock was consistently over the 100-mention mark, indicating a substantial social media following.

Notable comment from Reddit:

“They also released guidance that they'll make $50 in FCF this year before rates went even higher. You're buying an entire shipping company for $60 and change, and getting back $50 in year one alone in straight cash. Unless you think containership rates crash from ATHs to negative in the next 52, they're set to make absurd cash this year, and in an excellent position to do so for the foreseeable future even if rates return to normal.”

– JDinvestments

“I am very bullish on ZIM they have had fantastic last few quarters, they are cash-heavy and are expanding routes like crazy. The shipping sector is still in an upward territory and will continue like this until next year.”

– watchheroes

???? Smart Money Signal: Jim Simons of Renaissance Technologies purchased nearly 2.5 million shares of $ZIM in the second half of 2021.

Why $ZIM could be valuable:

The global container shipping market is expected to maintain a CAGR of 5% through 2026.

The Journal of Commerce forecast in May 2021 that while shipping is a cyclical industry, “demand will still grow faster (18 percent) than capacity (14 to 15 percent) over the next several years”. That equation points toward a sustained uptrend (though fluctuations are inevitable) in container shipping rates.

Over the long haul, McKinsey projects that container shipping demand will continue to grow for the next 50 years at least.

$ZIM’s charter-driven “asset-light” model avoids the heavy debt load and long-term commitment associated with buying ships and provides flexibility in meeting demand. ZIM has a reputation for high schedule reliability and innovative customer service, a substantial competitive advantage.

ZIM has generated rapid increases in earnings due to the post-pandemic surge in shipping rates and has effectively eliminated its debt.

$ZIM has delivered exceptional growth figures and valuation metrics over the last year, registering 209.7% revenue growth and 925.9% earnings growth in Q3 2021. This is largely due to a remarkable surge in container shipping rates.

Source: Bloomberg

The growth rates above in 2021 show that world merchandise trade grew 10.8% caused by a general shortage of container ships. However, the WTO predicts that merchandise trade will grow an additional 4.7% in 2022, indicating that demand will continue to be solid.

ZIM has produced exceptional results relative to peers in the shipping industry.

ZIM is a newly public company, despite its extended operating history. The Company held an IPO in January 2021. The IPO failed to generate interest, pricing at $15, below an already modest anticipated range of $16-$19, and the price sank 23% after trading began.

The stock price has risen dramatically from that point, but it’s rising from a very low base. That leaves the valuation at a very attractive level for a stock that’s been on an extended uptrend. Most stocks that have established strong buying momentum are pushing toward high valuations, but that’s not the case here.

$ZIM has promised to return 30%-50% of income to investors. The dividend in Q3 2021 was $2.50/share, for an enormous dividend yield of 16.4%. This yield is unlikely to be sustained and will moderate as shipping rates stabilize.

7 analysts currently cover $ZIM, with a consensus “Buy” rating and an average price target of $84.14, 20.44% higher than the current price.

What the risks are:

1️⃣Competition is intense. $ZIM competes directly with a large number of other shipping and logistics providers, including much larger companies like A.P. Moller – Maersk, Hapag-Lloyd, and Costamare.

2️⃣ Shipping rates will moderate. The 2021 surge in shipping rates is unsustainable and has already begun to correct. $ZIM will not be able to sustain the growth rate seen in 2021, which may lead some investors to lose interest.

3️⃣ Global trade is exposed to geopolitical risk. Conflict between China and Taiwan, in particular, could lead to sweeping sanctions or other trade restraints that could affect the container shipping.

Bottom line: $ZIM is a highly competitive player in a vital industry, leveraging technological leadership to generate operating efficiency and industry-leading results.

Franchise Group Inc. ($FRG)

Source: tradingview.com

Summary:

- Share price at the time of writing: $42.75

- Franchise Group is an owner and operator of franchised and franchisable businesses.

- $FRG currently operates over 3000 franchised or company-run business locations, primarily in the US.

- $FRG is focused on resilient retail businesses. There are currently six operating segments including furniture and appliances, pet supplies, nutritional supplements, and more.

- Franchise Group has established a solid acquisition record and shown consistent revenue and earnings growth since establishing its current business model in 2019.

What they do:

Franchise group was founded in 2019, when investment manager Brian Kahn acquired Liberty Tax, which was under pressure due to a CEO scandal, and merged it with rent-to own retailer Buddy’s. Khan then sold Liberty Tax and began looking for other basic, straightforward retail businesses that could be acquired for low prices and merged into a franchise-driven model.

Current Franchise Group businesses include:

- Buddy’s Home Furnishings is a rental/purchase and lease-to-own company focused on electronics, appliances, and furniture

- The Vitamin Shoppe is a retailer of nutritional supplements.

- American Freight is a retailer of furniture, mattresses, and home appliances. $FRG also purchased Sears Hometown and Outlet Stores and merged the Company with American Freight.

- Pet Supplies Plus is a pet supply retailer with 560 locations nationwide.

- Sylvan Learning provides personalized instruction, homework support, and exam preparation services.

- W.S Badcock is a furniture retailer with 370 locations primarily in the Southeastern US.

Sylvan Learning was acquired in Q3 of 2021 and W.S Badcock was acquired in the 4th quarter of 2021.

$FRG focuses on long-term investments in economically resilient niches with relatively low capital requirements. They target businesses in growing industries where the acquired company has the potential to expand market share.

Franchise Group’s strategy is to acquire these businesses, often at bargain prices, and use a franchise model to expand their presence without excessive capital cost. Franchise Group provides low-cost financing, operational assistance, support for developing a digital strategy, franchising support, site selection advice, and marketing assistance to help acquired companies maximize their potential.

???? Smart Money Signal: ???? Blackrock, the world’s largest investment manager, has taken an interest in $FRG and now holds almost 2.24 million shares, the largest single institutional holding.

Why $FRG could be valuable:

Franchise Group is a new company composed of established businesses and brands. There’s a clear management philosophy focused on buying known-brand retailers at discounted prices and expanding their operations through a low-capital franchise model.

Since the Company went public in 2019 it has made multiple acquisitions consistent with this business model. As with all retail businesses revenue growth in 2020 was constrained by the COVID 19 pandemic and the subsequent supply chain issues but remained despite that constraint, suggesting that growth can accelerate as pandemic restrictions are reduced and supply chain issues resolve.

$FRG has three potential growth drivers:

- Additional acquisitions.

- Adding stores in existing businesses.

- Improving same-store sales.

Franchise Group announced two acquisitions – Sylvan Learning and W.S. Badcock – in the second half of 2021. No further acquisition candidates have been announced but it’s reasonable to assume that the trend will continue.

$FRG will report Q4 FY2021 results on February 23, 2022. Year-over-year quarterly sales are expected to be up 69.7%. Earnings $0.97/share, beating the consensus estimate by $0.17 and increasing over 340% from the equivalent quarter in 2020.

Analysts expect 2021 sales to reach $3.16 billion, almost 457% above 2020. Sales are expected to increase 39% to 4.42 billion in 2022 as the impact of the Sylvan and W.S. Badcock sales hits the bottom line. Additional acquisitions could boost that further.

$FRG’s unique business model makes peer valuation comparisons difficult, but valuation metrics are impressive: the forward P/E is 10, PEG ratio is only 0.67, and the Price/Sales ratio is 0.7. The float is quite small at 27.1 million shares, so even a modest buying push can move the stock.

In January 2021 $FRG refinanced a package of 11% debt at 6.2%, substantially reducing interest expense, and further reductions are possible as profitability and creditworthiness grow.

$FRG announced a 40% dividend increase in December 2021. The dividend yield is now 5%.

Seven analysts cover $FRG, with a consensus “Buy” rating and an average price target of $61.71, almost 45% above the current level.

What the risks are:

1️⃣ $FRG has focused on acquiring retail businesses. These businesses were heavily affected by COVID-related restrictions and could be equally affected by any resurgence of the pandemic.

2️⃣ Like any acquisition-focused business, $FRG needs resources to close deals. This could result in significant debt or dilution, especially if an acquisition is unsuccessful or the Company is unable to integrate the acquisition.

3️⃣ $FRG is exposed to substantial “key man risk”. CEO Brian Kahn is clearly the driving force behind the company and its business approach, and if he were unable to continue as CEO the impact on the company could be considerable.

Bottom line: The Franchise Group is managed by a veteran investor with a clear, focused strategy and impressive capital allocation skills. The Company has established a solid growth pattern and seems well placed to continue and extend that trend.

That's a wrap!

Don't miss our next report. If you haven't already make sure to whitelist this email so we don't end up in your promotions folder. Not sure how to do it? Use this guide.